Understanding of oil price formation

Thematic page - selection of publications

The generally misguided long-term oil price forecasts;

Price formation and policy implications

This presentation discusses the generally misguided long-term oil price forecasts over the past 40 years, price formation and policy implications. Firstly, the failure of long-term oil price forecast is demonstrated. Secondly, the impact of the scarce nature of oil on price formation is discussed. Thirdly and fourthly, analyses from the fields of economics and political science, respectively, are reviewed. Fifthly and finally, the long-term boundaries for oil-price formation and policy implications are discussed.Key words: Oil price prognoses, multidisciplinarity, forecasting.

This is a lecture on a chosen topic (trial lecture) to defend a dissertation for the Degree of dr.philos, Faculty of Social Sciences, Department of Political Science, University of Oslo, March 12-13, 2009.

Published as and to quote (download):

Austvik, Ole Gunnar, 2009: The generally misguided long-term oil price forecasts: Price formation and policy implications. Working Paper no.186. Lillehammer: Lillehammer University College. 28. pages. ISSN 0806-8348.

BEYOND: MORE ON OIL PRICE FORMATION / PAST, PRESENT, FUTURE (selection):

Selection of publications directly on the topic (see also publication list at www.oga.no).

Seminars, courses on the oil market (selection):

- Austvik, Ole Gunnar, 2016: Hva bestemmer oljeprisen? Hvor hender det? nr.17. Norsk utenrikspolitisk institutt (NUPI),

- Austvik, Ole Gunnar, 2000: "Drivkreftene i oljemarkedet". Høgskolen i Lillehammer. Forskningsrapport nr. 50/2000. 50 sider.

- Austvik, Ole Gunnar, 1993: "Grenser for oljeprisen; Scenarieplanlegging som metode til å forstå utviklingen i oljeprisen". Sosialøkonomen nr.3 pp.21-29.

- Austvik, Ole Gunnar, 1993: A View on Economic Theory of Exhaustible Resources, Working Paper nr.89 - 1993, Oppland DH Lillehammer, 24 pages

- Austvik, Ole Gunnar, 1992: "Limits to Oil Pricing. Scenario Planning as a Device to Understand Oil Price Developments". Energy Policy pp. 1097-1105.

- Austvik, Ole Gunnar, 1986: Søkelys på mekanismene i oljemarkedet, NUPI-rapport no.97. 66 pages.

Selection of articles on various effects of and elements affecting the economic and political understanding of oil price developments - Petroleum management issues:

- Harvard University, 2016-03-07. "The Failure of Long-term Oil Price Forecasting.". Europe and the Geopolitics of Energy Study Group.

- Handelshøyskolen BI Norwegian Business School 2013-15: GRA 8194 Energy Economics and Politics.

- Austvik, Ole Gunnar, 2020: "Norsk energipolitikk. Statlig forvaltning, markedstilpasning og klimarisiko. Bokkapittel.

- Austvik, Ole Gunnar, 2018:: "Concepts of Geopolitics and Energy Security" - pdf - IAEE Energy Forum 2d quarter. pp.25-28.

- Austvik, Ole Gunnar, 2012: "Landlord and entrepreneur. The shifting roles of the state in Norwegian oil and gas policy.” Governance. An International Journal of Policy, Administration, and Institutions. Volume 25, Issue 2, pp. 315-334.

- Austvik, Ole Gunnar, 2007: "Staten som petroleumsentreprenør", Tidsskrift for samfunnsforskning VOL 48, NR 2. pp. 197–226.

- Austvik, Ole Gunnar, 1997: "Petroleum Taxation and Prices of Oil and Gas; Perspectives from the Supply Side". In (eds.): Aakvaag, T. & Mueller, F.: European Energy Supply at the Turn of the Century. Natural Gas and Electricity. Ebenhausen: SWP Stiftung Wissenschaft und Politik & Oslo: Europaprogrammet pp.86-112.

- Austvik, Ole Gunnar, 1996: "Avgifter og petroleumspriser. Tar forbrukslandene olje- og gassinntektene?" Sosialøkonomen nr.5/1996. pp.16-28.

- Austvik, Ole Gunnar, 1993: "The War Over the Price of Oil: Oil and the conflict on the Persian Gulf". International Journal of Global Energy Issues Vol.5, No.2/3/4, pp.134-143.

- Austvik, Ole Gunnar, 1991: "De strategiske petroleumslagrene (SPR) som oljepolitisk kriseredskap", Sosialøkonomen nr.1. pp. 2-7.

- Austvik, Ole Gunnar, 1987: "Exchange Rate Fluctuations as a Source of Disequilibrium in the Crude Oil Market. Oil Prices and the Dollar Dilemma. ". OPEC Review no. 4. pp.399-412.

- Austvik, Ole Gunnar (red.), 1987: Oljemarkedet og utenrikspolitikken, Internasjonal Politikk no. 5/6. NUPI. 228 sider.

Media on this paper: "Gas could burst Peak Oil theorists' bubble", The National, Abu Dhabi Jan 21, 2010.

"Peak Oil: When You've Got Nothing Important to Do", Al Fin Energy, Cayman Islands (U.S.), Feb 09, 2010

Remark: You are welcome to download, print and use this full-text document and the links attached to it. Proper reference to author, title and publisher must be made when you use the material in your own writings, in private, in your organization, in public or otherwise. However, the document cannot, partially or fully, be used for commercial purposes, without a written permit.

Ole Gunnar Austvik:

The generally misguided long-term oil price forecasts; Price formation and policy implications

1. Introduction

Some background for choice of subject for this lecture was illustrated last year. Early July 2008, some 8 months ago, the price of crude oil reached an historical height of 146 dollars per barrel ($/bbl). Many analysts expected it to rise to 200 $/bbl quite soon. Albeit not everybody claimed the price to become that high, close to everyone expected it to remain high in the short-run and rise further in the long-run. Only very tiny voices said last summer or in the year before, in 2007, that it was possible at all that the price of oil could be as low as 40 $/bbl later this winter, or say, ever.

The story is not new. Over the past 40 years, short- and medium term oil price forecasts have almost never foreseen discrete shifts in the price. Long-term forecasts (which in this case are considered to be 3-4 years and more) have continuously been wrong. Decisions about investments in oil and gas resources as well as in renewable energies are taken on the basis of these perceptions. Policy design in oil consuming and producing countries are chosen based on assumptions of how energy markets in general, and the oil market in particular, are thought to develop.

This presentation is about the misguided long-term oil price forecasts, price formation and policy implications. At the end I will make some remarks on what we can learn from it as a case in International Political Economy (IPE).

2. The failure of long-term oil price forecasts

Let us start with taking a look on forecasts made over the past 10 years, and then turn to the history of forecasts in the 1980s and 1990s.

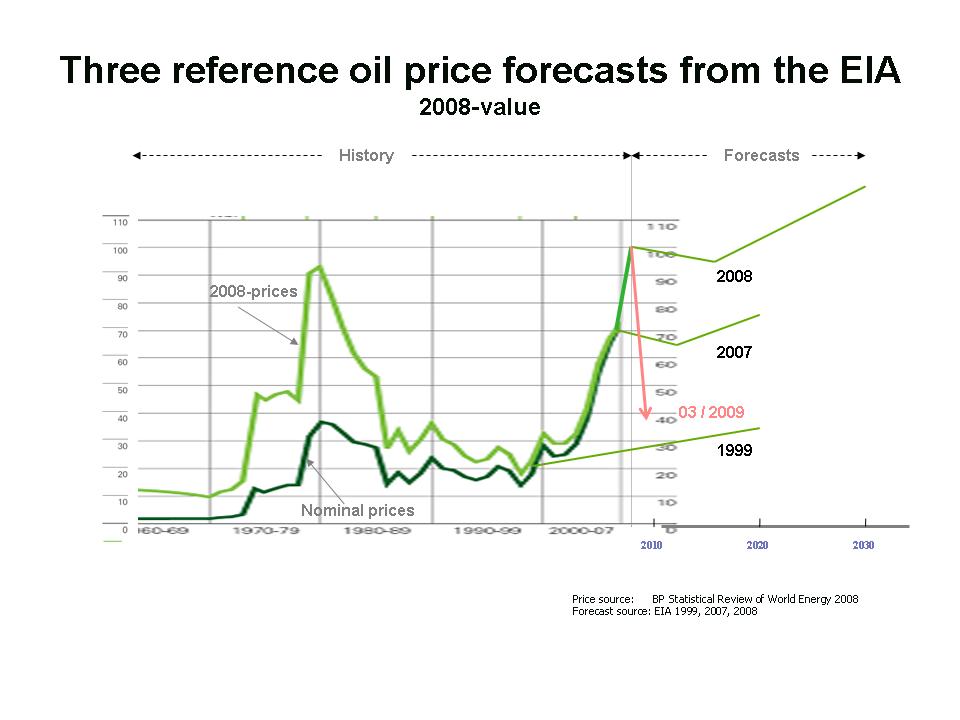

As a representative source for the prognoses over the last 10 years I choose those from the Energy Information Administration (EIA), which is the statistical office under the US Department of Energy (DOE), not to be confused with the International Energy Agency (the IEA). The EIA is not worse or better in forecasting than any of the others, just representative and authoritative. Note that in the graph nominal oil prices are shown as dark green color while real prices in present-day money is shown as the higher, light green color. All forecasts here are shown and referred to as yearly averages in real 2008-valued prices.

The three forecasts taken from this decade are from 1999, 2007 and 2008. Some spreads around the medians were given, here are only the reference forecasts shown.

In 1999, ten years ago, the yearly average of the oil price was around 21$/bbl in today’s money. The reference forecast for 2009 was some 25-30 $/bbl and some 36 $/bbl for 2020.

In spite of this expectation, in 2007, current prices had reached some 70 $/bbl, and then the reference forecasts were changed for 2020 to some 80 $/bbl.

Only one year later, in the beginning of 2008, the expectation was again changed as current prices passed 100 $/bbl. The reference forecast for 2009 and 2020 was then 100 $/bbl, rising towards some 130 $/bbl in 2030.

The recent drop in oil prices was not included in any of the forecasts over the decade.

Very similar forecasts were made by a number of other institutions, agencies, financial institutions, individuals and others, including in Norway. The expectation in every year has been that prices should rise in the future, whether the initial price is 20 or 100 $/bbl or somewhere in-between.

This type of consensus forecasting is not new. Going 40 years back in time, consensus in industry, government and academia did generally not foresee the first oil shock in 1973. It was an established fact at the time that the low pre-crisis price of oil should remain low. Interests in forecasting the price were moderate. Hence, the first oil shock came as real a shock to both the industrialized and developing world, being unprepared to a new global economic environment with high energy prices.

After the first shock and the stagflation crisis, and reinforced by the second price shock in 1979-80, oil prices became an important issue in international affairs and administrative and regulatory reform. With the structural crisis and its acknowledged importance, the number of price forecasts increased substantially.

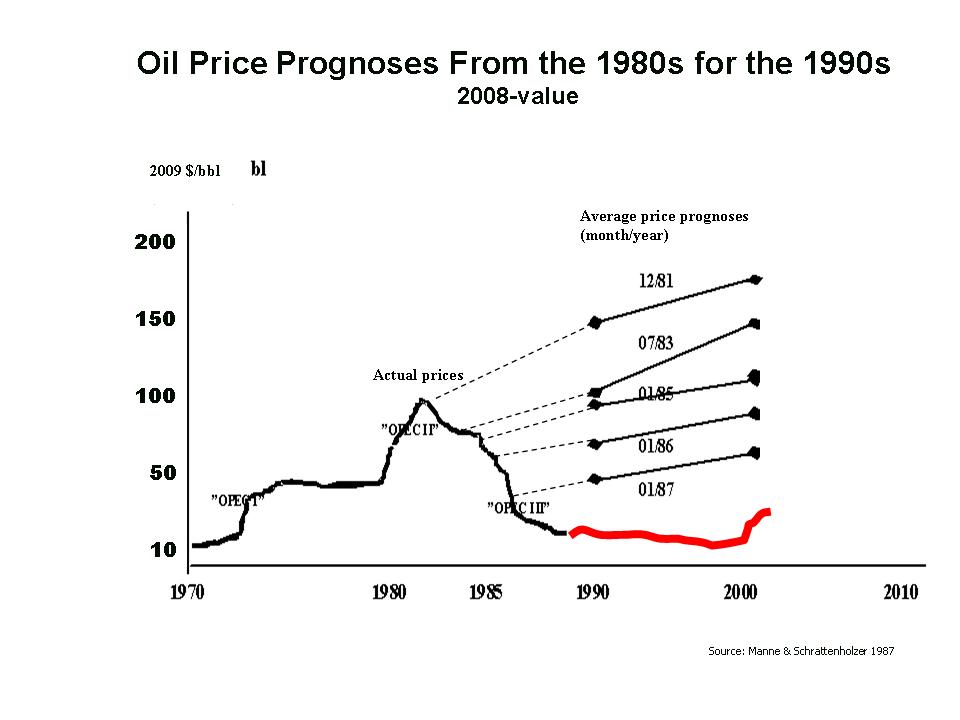

In the 1980s, in what was called the International Energy Workshop performed by Allan Manne at Stanford University and Leo Schrattenholzer at the IIASA institute near Vienna, 3-400 hundred forecasts from around the world about oil prices in the 1990s were gathered. The respondents were economists with comprehensive mathematical and computerized models, political scientists, journalists, ministries and companies, with very different backgrounds and analytical approaches. The workshop found that each forecaster made quite the same expectations as the others about the future, independently on methodology used: At any point in time, prices were by all expected to rise in the future from the at any time prevailing price level.

According to the 1981 forecast, when the oil price in today’s money was some 90 $/bbl (nominal 35-40 $/bbl) – at the level of last years average price - oil prices were expected to rise to the range of 150 $/bbl in the 1990s.

As prices nominated in US dollars gradually dropped after 1981, the expected level of the future price also dropped, but the upward trend was maintained.

Even after the price collapse of 1986, in January 1987, when prices were in the low 20-ies $/bbl in today’s money, prices in the 1990s were expected to rise to some 50-60 $/bbl.

Looking at the forecasting period 1981-1987 the price was expected to be somewhere in the range of 50-150 $/bbl in the 1990s in the value of today’s money depending on when the forecast was made during only these 6 years.The only price level nobody anticipated in this period was the one that actually occurred in the 1990s. None of the forecasters imagined that the price could end up as low as at a level of nominally 15-20 $/bbl, or 20-25 $/bbl in today’s money.

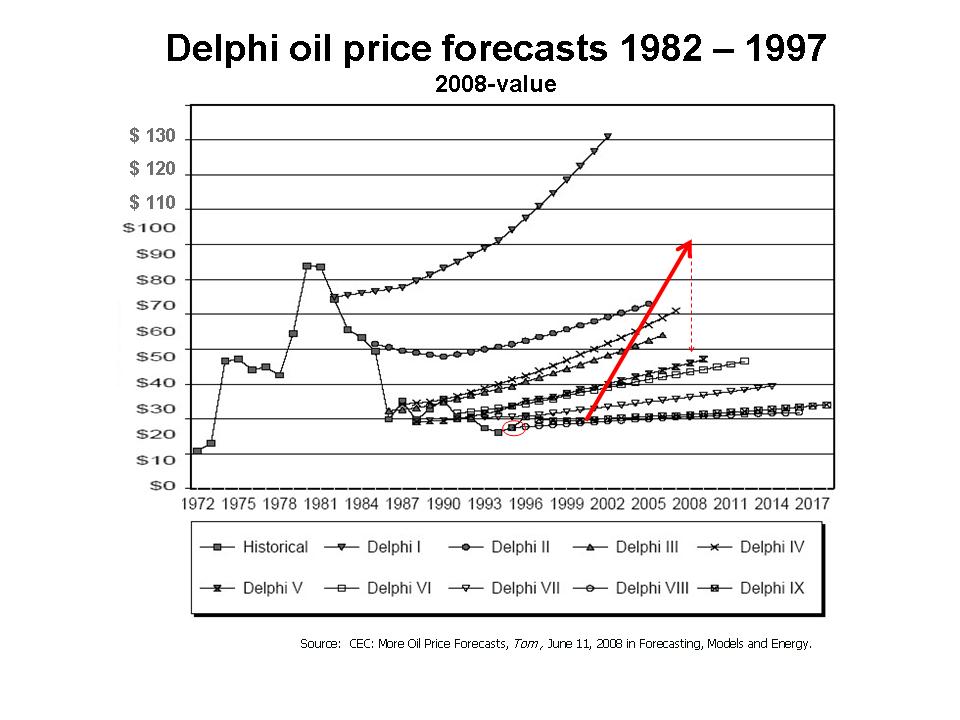

In the 1990s when prices stayed relatively low, expectations for rising prices were maintained, but at a gradually flatter level. The last one in this Figure is showing the expectations from 1997 in present-day prices. It is assuming a price only slightly higher in 2017, rising from the mid-20-ies to somewhat above 30 $/bbl, closing the ring to the EIA forecast of 1999 that I showed earlier.

As in the 1980s, none of the forecasters in the 1990s could imagine the price that actually occurred in the following decade. This time it was not a drop in prices, but a rise to 100 $/bbl.

Thus, over the last three decades the yearly average of the oil price has varied between 12 and 100 $bbl, fluctuations has covered a range from nominally 9 to 146 $/bbl, and the forecasts for 2010 (next year) between 20 and 150 $/bbl.

In no periods has the forecasts included any of the significant changes that has taken place in the market. And even if the failure of long-term oil price forecasting has been well-known and documented at least since the 1980s, economists, political scientists and others continue to make them, and make recommendations and decisions based on them, on company as well as on state and international levels.

3 Oil as a scarce resource

One important reason for people independently of theoretical or practical approach to believe in rising prices over time is the fact that oil geologically is a scarce resource. Oil (and natural gas) differs as non-renewable resources from renewable resources in that their supply is limited to a relatively few places in the world. As resources are exploited, remaining reserves are reduced. What is extracted today cannot be extracted tomorrow.

This geological fact easily leads to the conclusion that as resources are extracted; prices of the remaining reserves must be pushed up.

The “Limits to Growth” way of thinking from the 1970s, as an example of neo-Malthusian theory, supported the view of scarcity and rising price expectations. So far however, neither Malthus more than 200 years ago, nor the thinking of the 1970s, has proven to be fully correct.

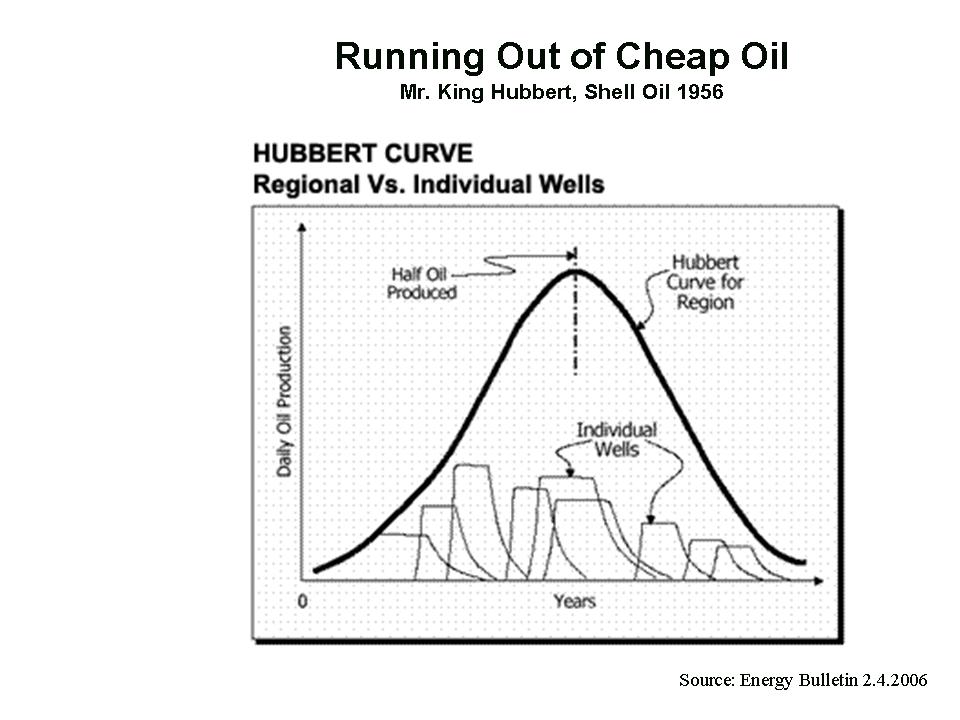

Present-day peak-oil enthusiasts have over the last years gathered great support for this type of view. The peak-oilers lean strongly to the so-called Hubbert curve presented in a paper by the Shell geologist Mr. King Hubbert in 1956. It posits that for any given geographical area, from an individual oil-producing region to the planet as a whole, the rate of petroleum production tends to follow a bell-shaped curve. Given the shape of the curve, the point of maximum production based on discoveries, production rates and cumulative production is determined. Before the peak the production rate increases due to high discovery rates. After the peak has been reached, production declines due to resource depletion and lower discovery rates. The peak-oil theory has shown some evidence in terms of production figures. Fore example, the US lower 48 states peaked in the early 1970s, as predicted by Mr. Hubbert. Norway’s oil production peaked in 2004, and production is continuing to decline.

Oil reserves are however an ambiguous notion. Sticking to the term “proven reserves”, it depends inter alia on costs, prices and technology in addition to the estimates made geologically for each field and region. While for example relatively high-cost, but huge, Canadian oil sand fields were excluded from the term until about 2004, the high prices has made them more profitable and they were consequently included in commercial (proven) reserve figures thereafter. With the lower prices now, much of them might however disappear again from commercial reserve figures.

Using these terms for the analysis, the US has had a production horizon of 8-10 years since the 1960s. Norway has had a similar 8-10 years production horizon for some years now. But few believe we will actually run out of oil that fast.

On a global scale, there are consequently disagreements whether the rate of production has already outpaced the rate of discoveries and field expansions, and hence already peaked, or whether the peak will come some time in the near or distant future in the century we are into now.

The next question is then what does economic and political theory tell us about oil-price formation of the scarce resource?4 Economic analyses

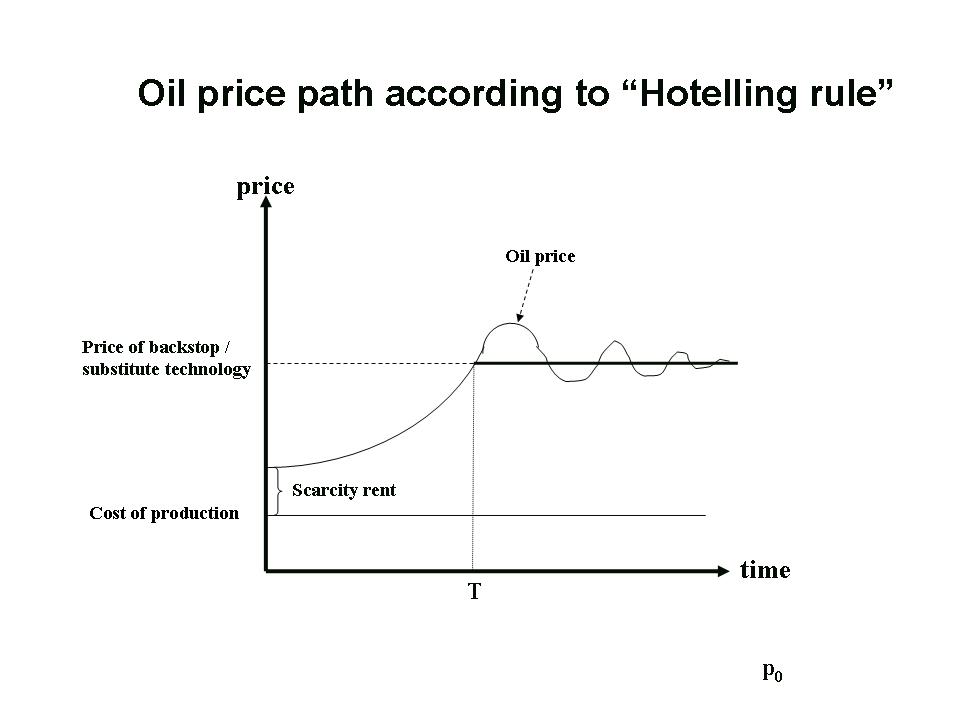

Economic theory of exhaustible, or non-renewable, resources, in the most simplified version, tells that the price of oil will rise with the rate of interest due to its scarcity and oil producers' rational behavior in dealing with this scarcity. This understanding is known popularly in academia as the Hotelling rule, according to Harold Hotelling’s article from 1931.

After some time T, however, the theory states that the price of the exhaustible resource will converge towards the substitute, or back-stop, price. It takes time to introduce the backstop-fuels and the resource price may therefore pass the substitute price for a while, until sufficient amounts of the alternative fuel(s) have reached the market. This is because, on the demand side, short- and medium-term price elasticities are significantly different from long-term price elasticities. Thus, when oil prices are high, they start a row of reactions in markets for both oil and its alternatives, which in their turn has long-term implications for the demand and price for oil.

1. Consumers save more energy.All these reactions take time, from several months to many years, depending on a number of factors.

2. Consumers switch to alternative energy sources.

3. Consumers with low willingness (or ability) to pay must reduce their economic activity, and hence energy demand.

4. Suppliers of alternative energy sources, both renewable and non-renewable, intensify their efforts to provide more. More investors are attracted to the energy sector in general as a place for opportunities.Therefore, any short-term price of oil cannot in itself be used as a signal of a long-term trend towards neither lower nor higher prices.

An intriguing question is however what the backstop price is, as it will only be observed some time after it is passed by the price of the exhaustible resource, or here: oil. And it changes over time, as this graph is showing:

Professor Maurice Adelman at MIT has for a long time been a strong advocate for the view that economic and technological developments would lead to a decline, and not a rise, in petroleum prices over time. More resources will be found, and technological changes will be introduced in production, transportation and consumption, and together with lower priced substitutes they will limit petroleum prices. Even if resources are exhaustible in geological terms, and limited periodically due to political, technological or infrastructural constraints, they need not be so in economic terms in the long-run, Adelman argues.

Thus, the rising price scenario is only true in the ceteris paribus case. If, for example, reserves are upgraded sufficiently, demand becomes more price-elastic, economic growth declines, technology becomes more efficient, and cheaper substitutes introduced prices should be revised down.

It is consequently debated to which extent non-renewable petroleum resources should be considered scarce or abundant in economic terms in the long-run. While the simple understanding of the Hotelling rule and peak-oilists often says “yes”, the minority like professor Adelman maintains that prices in the long-run will decline, in spite of their exhaustible character. One question in this very different world of perceptions is how supply is determined and whether oil producers will extract resources fast or slowly.

Economic theory expects producers to behave rational and optimize scarcity rent and hence wealth over time. By moving production between time periods to achieve this optimization, prices would, again under simplified assumptions, increase with the rate of interest, until it reaches the substitute (or backstop) price.

But is this a good description of oil producers’ behavior? Are producers collectively actually optimizing wealth in this long-term rational economic manner, or are other considerations and constraints considered more important in order to understand the supply side of the market?

Alterative explanations emphasize some other aspects, such as the Target Revenue and the Property Right theories. Both had substantial support in the 1970s and 1980s.

Most focus has however probably been attached to how international market power on the supply side affect prices, especially producer cooperation in the Organization of Oil Exporting Countries (OPEC).

4 Political analyses

OPEC market power has been studied both from an economic viewpoint and via various political models. In economics, models have been developed to discuss how producers may gain a monopoly rent in addition to the scarcity rent in the market by the means of different forms of collaboration as part of their optimization. The discussions within political science put more emphasis on political aspects as motivation for different forms of tacit and non-tacit collusion and conflicts.

One game theoretical aspect in a realist perspective is that production reductions in OPEC countries also benefit other countries, which implement no reductions. Combined with disagreements as to which price level is the right one, this is an important reason for the disagreement within OPEC, and between OPEC and non OPEC countries over production rules and quotas.

This is comprehensively discussed in Dag Harald Claes’s dissertation, and later book, on “The politics of oil producer cooperation”.

OPEC was considered to change the regulatory regime of the oil market in the 1970s. However over time, the organization has had difficulties in maintaining a price fixing policy when pursued too strongly.

Market mechanisms limit the maneuvering room for OPEC policy over time. If they exceed the limits the market can sustain the organization may experience that they “come in as a lion and go out like a lamb”. This was partly the result of the organization’s high-price policy of the early 1980s.

Policy is however also important on the demand side. On national levels energy policy in consuming countries have the potential to influence a number of demand factors over time. Regulations, subsidization and taxation are important political instruments.

In some countries energy policy has however largely been limited to influencing the operation of the markets by regulatory authorities over the past decade, such as in the UK and the US.

Tendencies for replacing only regulatory policies with more interventionist policies are however seen following the high energy prices. According to neo-functional approach economic change deduce in spill-over to political and institutional change.

The EU and the new Obama administration in Washington have expressed plans for actions that more rapidly increases the role of renewable energy sources and speed up efforts for energy savings. Their challenge is to create and develop institutions, political instruments and ideological acceptance for achieving these goals.

The possible shift in policy tends to lower oil demand compared to previous expectations and makes demand more elastic in the future. This could improve market stability and possibly also lower substitute energy prices, and hence the maximal sustainable level of the oil price, faster than market actors would do it without intervention.

As on the supply side, some political goals can best be achieved by international cooperation also on the demand side. The International Energy Agency (IEA) was established on the initiative of President Nixon and his foreign minister Henry Kissinger as a reaction to the first oil shock in 1973/74, to counteract OPEC's support for what was considered unreasonable high oil prices thereafter. The IEA represents an international body coming up as an intergovernmental approach to global energy markets.

A main task of the IEA is to help reduce the sensitivity and vulnerability of member countries in their dependency on imported fossil fuels. Coordinated efforts have stronger impacts in the market on the demand as on the supply side. Also the IEA has shifted attitudes from rather interventionist in the 1970s to liberalist in the 1990s.

It is important how the organization will work in the future together with its member countries, and also whether it will expand its membership area to include the growing new economies in Asia in order to remain relevant as a coordinating actor on the demand side.

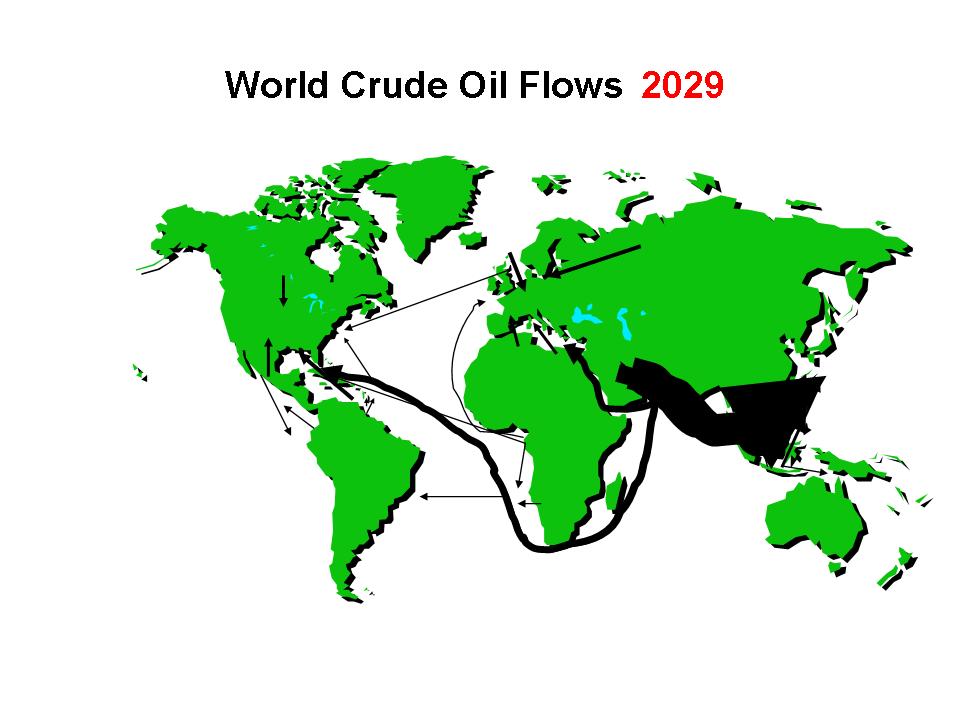

There has also been a lot of emphasis on the situation in the Middle East and, in particular the Persian Gulf area, and its impact on the oil market. Many scholars in political science have in their efforts to understand the oil market concentrated primarily on Middle East internal and external affairs.

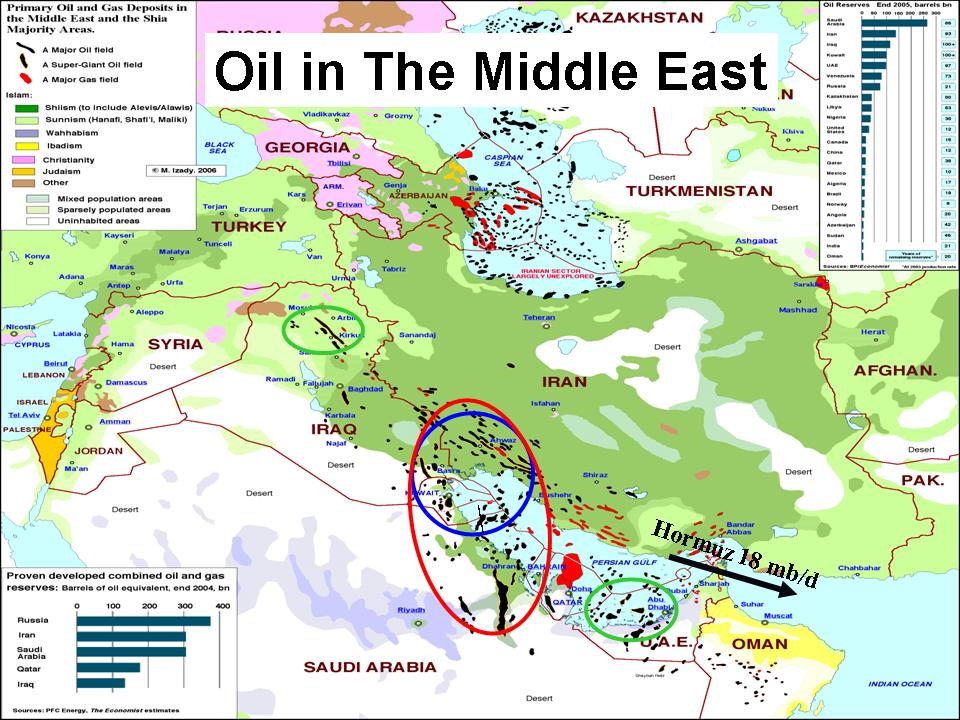

The reason for this emphasis should be clear from this map. If you make a circle with a 200 km radius with the centre in the bottom of the Persian Gulf you find some 50 % of world proven reserves. This radius is not longer than the distance between Oslo and Lillehammer.

In the Persian Gulf this small area with all its oil is divided between 4 countries: Iran, Iraq, Kuwait and Saudi-Arabia. Several wars have been fought on top of these fields; foremost the Iran-Iraq war in the 1980s, the Iraq-Kuwait-War in 1990-91, the US-Iraq war since 2003. The troops from the host countries plus American, British and other military forces are literally standing on top of the oil fields.

If we expand the circle and change it to an ellipse of 400 km from the centre to its furthest outskirt, the largest oil-field in the world, the Ghawar field is included. Together these reserves represent 2/3 of proven world oil reserves. As a comparison Norwegian reserves are expected to represent some 1.2 per cent of the world total.

When we add that to get this oil out of the region, as much as 18 million barrels has to pass through the Strait of Hormuz on average every day (which is perhaps 10 supertankers), we see the geopolitical oil picture of the Middle East. The exports represent some 1/3 of world total.

The countries in this oil-rich area have different pricing objectives in their oil policy. The conflicts between the doves (Saudi Arabia, the Emirates and Kuwait) that want lower oil price than the hawks (in Iran and Iraq) are well known, and have been a major reason for endless discussions about quota regulations in OPEC and cheating on the quotas assigned.

The reason for these differences in pricing policy is obviously not only grounded in different views on how to optimize resource wealth, but different needs in domestic economies, internal / domestic conflicts and rivalries, conflicts between the countries and different relations to the West, to mention some. To understand these political issues is crucial to understand degree and form of political stability and production developments. The outcome is also essential for production regulations, regulatory behavior of OPEC and their relations to the consuming world, Western and now also Eastern.

Another geopolitical fact is namely that oil from the Persian Gulf area is not anymore going primarily to the US and Europe, but to Asia. There has been a trend since the early 1990s that demand growth to a much larger extent comes from developing economies in countries like China and India. The balance between OECD and non-OECD demand for energy is shifting towards the new economies, reflecting their increased economic significance in the world economy. The consensus expectation 20 years ahead in time is that the trend of increased significant of Asian economies in world economy will continue. Asian countries should be expected to play an increasingly more significant role on aggregated demand side behavior in the oil market, as well as in Middle East politics in the future.

Because the oil market is global the balance between energy consuming Asian countries and producing Middle East countries will affect all participants, including Norway as seller and the EU and the US as purchasers, even though we all live far from these areas.

How does the degree of political tension in the PG and market tightness affect the prices?

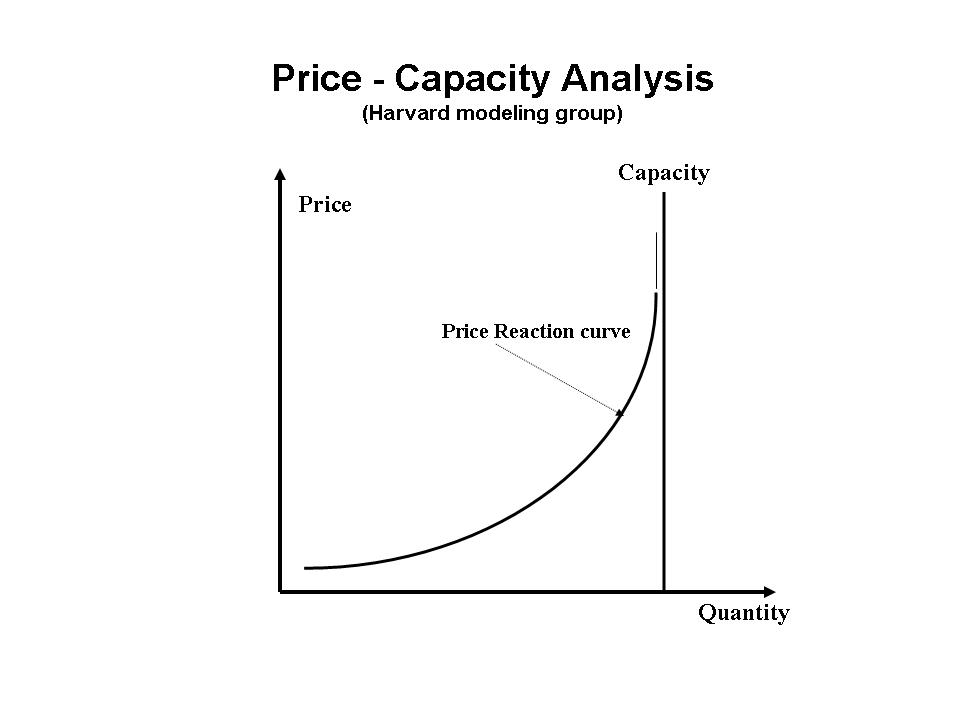

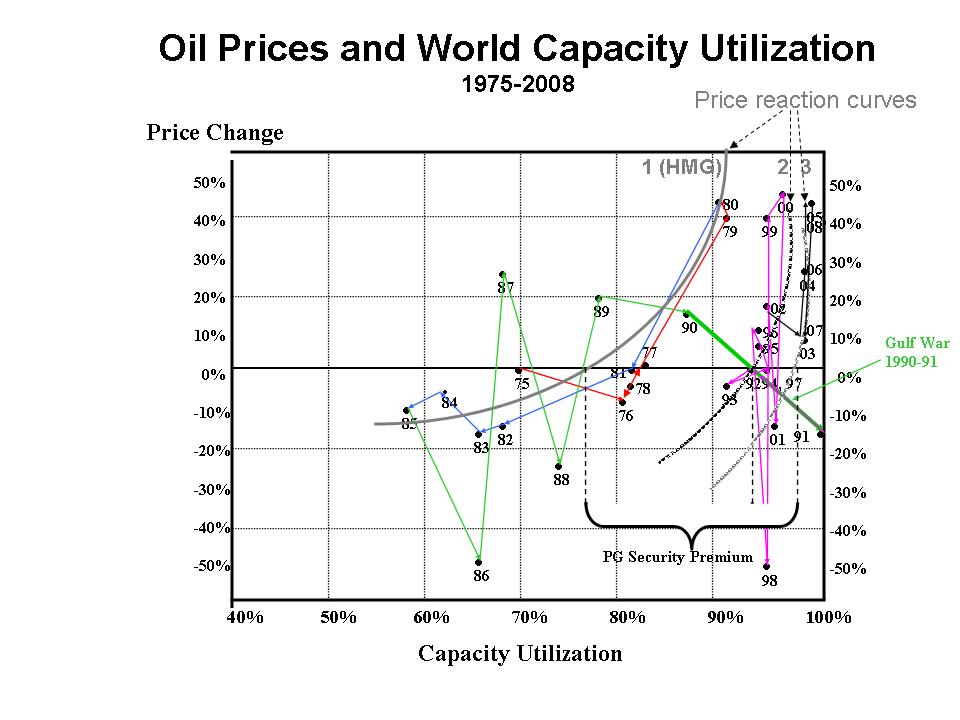

A model for how to understand the relationship between the tightness of the market and reaction on oil prices was developed by what was called the Harvard modeling group (Harvard energy studies) in the 1980s. The tightness in the market was in this approach understood as how much unused capacity there is (meaning practically in OPEC or PG countries) at any point in time. 1974-1990: The group found that in the period after the first oil shock and up to the Gulf war (i.e. the period 1974-1990) prices increased when capacity utilization passed some 80 per cent of total. We see here how prices increase with higher capacity utilization up to the second oil shock in 1980. Then they decrease in line with gradually more capacity made available until capacity utilization in 1985 falls below 60 %. After that, demand again increases, capacity utilization increases as well as prices. Observing these facts, a price reaction curve to degree of capacity utilization was constructed (no.1).

1991-2003: In 1991, a dramatic shift in this reaction curve took place. With a 100 per cent capacity utilization in 1991 prices were actually dropping. After the Gulf-war in 1991 prices fluctuated but remained at a relatively lo level, in spite of a capacity utilization of more than 90 %.

The interpretation is that the Gulf-war introduced substantial US, British and other troops in the area. Oil supply from the area was by market actors considered more stable when this fact was evident as compared to before, and the chance of a supply shock caused by political events in the area perceived reduced.

The control gave se security premium on prices. The market could sustain higher capacity utilization without pushing prices up.

The new price-reaction curve (no. 2) illustrates that prices continued to react to market tightness after 1991, but at a higher degree of capacity utilization with the perception of greater stability at the supply side.

2003-NOW: After the American invasion of Iraq in 2003 the market has generally become even tighter, with only some extra capacity available mainly in Saudi Arabia. Prices have generally increased every year, but not as much as they would with similar capacity utilization as in the 1980s. The price reaction curve (no. 3) is now even closer to full utilization.

Turing it around: As demand decreases prices can fall dramatically in such a situation. This is what happened in 2008.

The graph indicates that price reactions to changed capacity utilization or market tightness are different under different political situations in the PG. It translates to some extent the degree of political stability in the area into a reaction in prices.

The present situation, not peace but perceived physical control, may indicate that Middle East politics has less significance for oil prices today compared to in the 1970s and 1980s. Production figures however do, as they do from any other place in the world.

Renewed instability that threatens or have a perceived potential to threaten, the supply of oil may, such as a conflict with Iran or a chaos in Iraq if the US is leaving the country, may however again change the price reaction curve.

6 Long-term price boundaries and policy implications

To sum-up: Nearly identical type of forecasts have been predicted when the initial price is 20 $/bbl, as at 65 $/bbl, or 100 $/bbl, whether the forecasts are made in the 1980s, the 1990s or over the last decade, when it peace or war in the Middle East, whether economic growth is high or low and whether prices nose-dive or sky-rocket, whether world politics is calm or not.

The forecasts are generally not based on proper theoretical grounds, as discussed. Another MIT professor, Michael Lynch, phrased in 1992 in his paper “The fog of commerce” them to be result of psychological and institutional factors.

Relying on extrapolation and consensus about price consequences of resource scarcity is obviously the easiest method. Deviation from this consensus requires an at least implicit public presumption of superiority over the great majority of other forecasters, which is not only difficult psychologically, but can also obviously be a very poor strategy.

Referring to the Japanese proverb; “the stake that sticks out gets hammered down.”

After studying this phenomenon for more than 25 years now, I think however we should acknowledge that the oil price should not be attempted forecasted in the ways that has been done over the past decades, and decisions should not be made on basis of them.

Does that mean that anything can happen in the future in terms of prices, regulatory schemes and institutional change?

In the very, very long-term: probably largely “yes”.

But when long-term is understood as a decade or two, we can say more than that. In this time perspective there are possible as well as impossible paths for the price of oil based on economic and political analyses discussed.

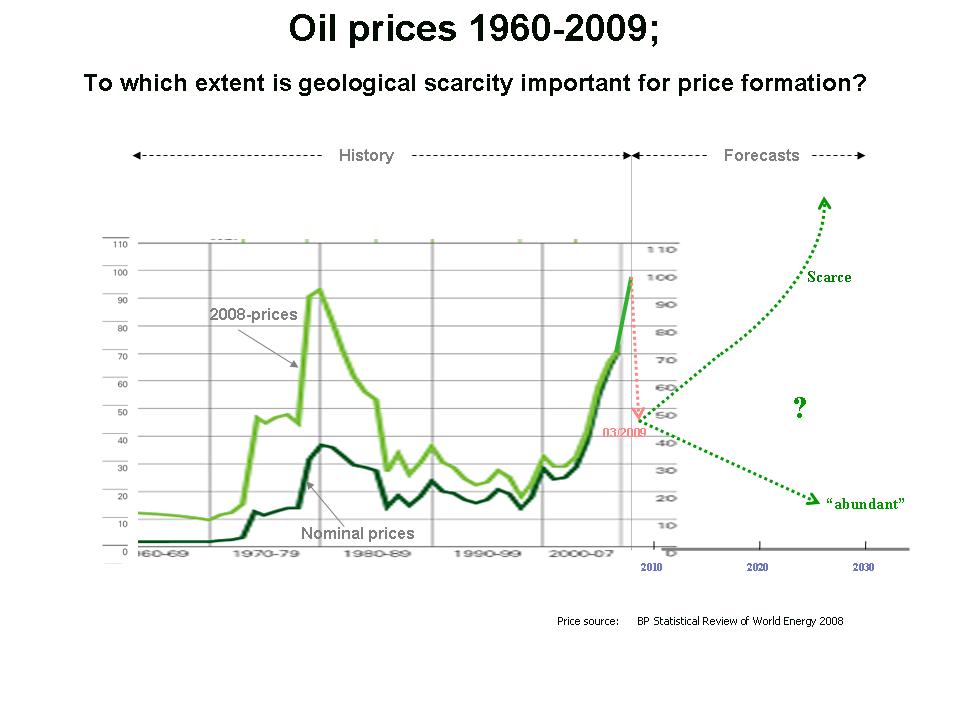

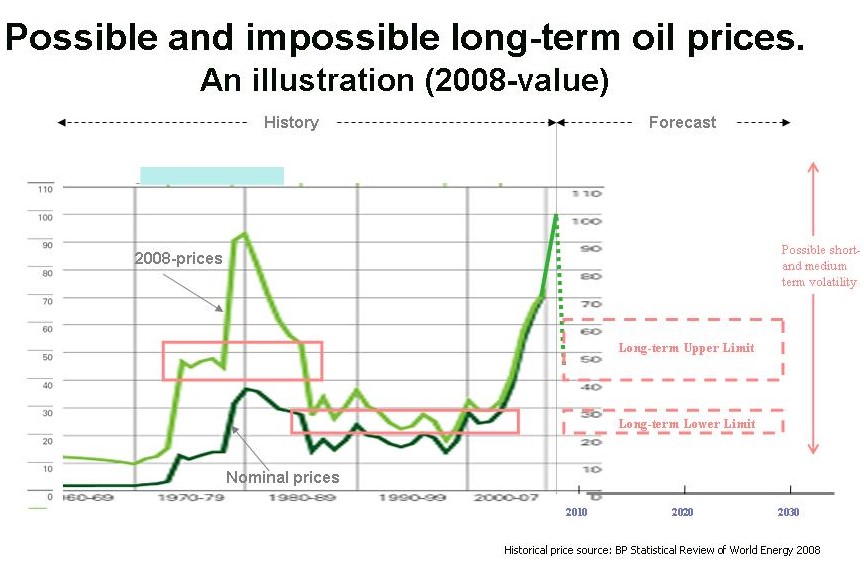

To illustrate: In the 1970s OPEC and political events brought the price of oil up from 10 to some sustained 40-50 $/bbl in today’s money. In the 1980s, the second oil shock brought the price above 90 $/bbl and OPEC tried to maintain this price level by quota regulations, helped by general unrest in the Middle East and the war between Iran and Iraq. This proved to be impossible. In 1986 the price collapsed, partly of this reason.

Without any dominant or specific regulations, the price in the 1990 stayed at level of 20-30 $/bbl in today’s money. The tight market by the turn of the century, caused by increased consumption and almost no net increase in global production capacity, brought the price high again thereafter, helped by the events of 9/11 and the Iraq war.

But again the price was too high to be sustained and collapsed again last year, probably earlier than it would without the financial crisis. If OPEC again tries - and succeeds - to maintain prices at 70 $/bbl or higher, as is discussed in the organization, they probably are redoing the mistakes from the 1980s.

To find such long-term limiting bands for the oil price is obviously a challenge. But even at the level of this discussion they indicate narrower boundaries than the accumulation of the myriads of long-term price forecasts covering a range from 20 to 100 $/bbl over the three past decades.

This graph illustrate them as being between 20-30 and 40-60 $/bbl. In the short- and medium term it is possible they can be well below and above these limits. These fluctuations must be understood by partly other tools than the long-term developments are understood.

As already mentioned, short term prices however do not indicate any trend towards neither higher nor lower prices in the future.

The limits to oil pricing also describe limits to and opportunities for industrial and political decision making and effects of exogenous events, different than the view that prices can continue to rise forever or to be sustained at unsustainable levels provides. I mention only some:

• At the international level, OPEC market power is over time limited by what the market can sustain. If we disregard that OPEC in extreme situations may temporarily succeed in reducing production and bring prices up to unsustainable levels for periods of time for political or other reasons, the organization can first of all, albeit not only, function as a price stabilizer. This parallel the stabilizing function of governments in national economies, that Keynesian macroeconomics introduced after the Second World War.In this short presentation I have discussed various economic and political approaches, albeit not nearly all, to explain why actual oil prices have strongly deviated from long-term oil price expectations. The suggested changed perspective of what may and what may not happen, rather than forecasting a reference price path with some spreads around it, has several implications for long-term industrial and political decision making.• Wars in the Middle East may have serious short and medium term effects for the oil market, but in the long-term their effects are more limited;

• Physical control of Middle East oil reserves can help consuming nations to better maintain stability in oil market supply, but over time not to limit prices to remain at the lower level. Political stability could however make prices more stable on the higher level, without the disturbing shocks. Political stability can on the other hand also – and perhaps better - be achieved by other means than physical control.

• Active energy policy in consuming countries in the form of encouraging faster development of alternative fuels, diversification, flexibility and energy savings has strong potential of shorten the period when short- and medium term high prices are sustained. It can also lower the upper limits of a sustainable long-term oil price.

This has already happened to some extent after the first oil shocks, but should be politically have been supported more, especially in low price periods as in the 1990s.

These long-term effects should be the obvious and realistic goals for consuming countries. They can be done by domestic measures, but should be internationally coordinated to maximize their effects, such as through the IEA.

International institutions and national energy policy are established, but their content varies with the general political ideology in this as in other fields. Generally, time perspectives for all participants have so far been too short to reflect the fundamentals really to take into considerations for political decision making.

• For an oil company like Statoil: Investments in Albertan tar sand field, and in the Shtokman field in the Barents Sea, may not be commercially profitable, at least not before technology is changed, disregarding environmental and other problems;

• Price volatility first of all in the short- and medium term, but also within the limits of long-term, underlines what a good idea it is for oil exporting countries to decouple revenues and expenditures through a Petroleum Fund buffer;

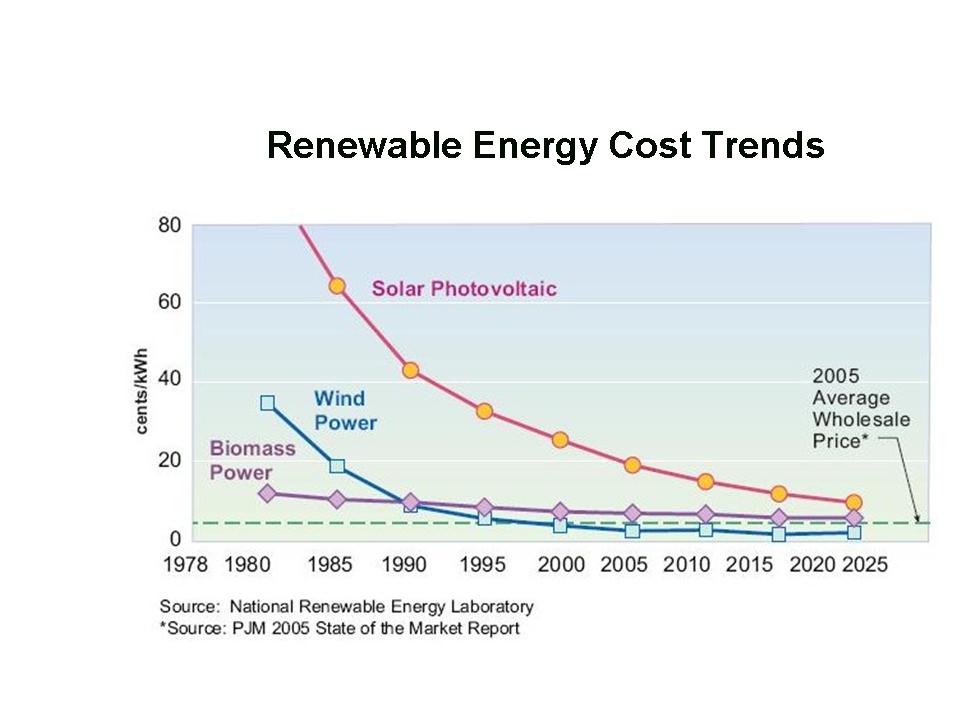

• Investments in renewables should be based on equivalent oil prices of maximum 50 $/bbl. But note that prices for longer periods may remain lower than that.

• The winner will be the technological breakthrough in the production or usage of one or more of the renewables, that can bring their prices down to an equivalent of an oil price of 20-30 $/bbl. Obviously taxes and subsidies could alter these relative limits of profitability as part of consuming countries’ energy policy.

To help improve the understanding of systemic and structural uncertainty and the adaptation to it, a proper integration of economics and political science disciplines (and others) is generally necessary, not only to refine one of them, as discussed also in my thesis. It is also necessary to lower ambitions at the detailed level in order to improve understanding on a more aggregated level, and to find more sophisticated ways of adapting to interdisciplinary uncertainty.

-

In my view, the empirical studies of oil price forecasting is applicable not only to the oil market and energy policy, but to more aspects of policy making and the understanding of IPE.

The types of consensus opinions of more or less exact predicting what the future might look like are found in many areas.

One example that is focused heavily these days; even if the petroleum fund is a very good idea, as mentioned, its investment strategy might have looked different if the systemic uncertainty in financial markets were understood better.

By including an inter-disciplinary perspective of the uncertainty of putting so much money in international financial papers, institutional and regulatory change and its possible incapability of controlling the market should be included in the assessment of what the future may look like. The longer the time perspective the more likely it is that a discrete or dramatic shift will occur in a market.

Including an interdisciplinary approach to understand this uncertainty, would probably lead to a more diverse investment portfolio than to put all in international financial papers (being stocks or bonds), such as leaving more oil in the ground and a stronger policy to upgrading the society at home and its infrastructure (widely defined).

-

Consensus is over time often shown to be of relatively minor value when major “unthinkable” discrete changes take place. This consensus is however based on neither empirical evidence nor theoretical models either from economics or political science or other. It appears, as Michael Lynch argued in 1992, to be result of psychological and institutional factors.

The type of consensus thinking and decision-making will however probably continue, doing the same mistakes as before, in spite of me having held this lecture today.

top of page

MAIN PAGE, PUBLICATIONS, MINI C.V., LINKS,ABOUT