|

Ole

Gunnar Austvik:

"Norwegian Petroleum and European Integration". Chapter 9 in B. Nelsen (editor): "Norway and the European Community; The Political Economy of Integration", August 1993, Praeger Publisher page 181-209. CT Westport, Connecticut, USA. ISBN 0-275-94211-2. |

Norway is producing oil and natural gas at a record pace. In 1991, Norway produced almost two million barrels of oil per day (mb/d), incl. NGL, and twenty-five million cubic meters (BCM) of gas for a total of 115 million tons of oil equivalent (mtoe), an all-time record. Production is expected to increase further in the 1990s, with oil production passing 2.3 mb/d and gas production reaching 50-60 BCM/year.

Norwegian oil and gas is growing in importance in international energy markets. Norway produced more oil in 1991 than Kuwait before the 1990 Iraqi invasion. With oil production declining in the former Soviet Union, Norway may soon be the largest energy exporter in Europe, and one of the largest in the world. Furthermore, energy attracts for Norway more world attention than any other issue besides military security.

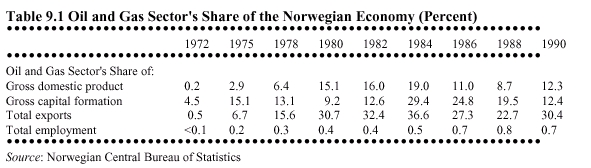

The petroleum sector is also playing a more significant role in the Norwegian economy. Today it accounts for about 14 percent of Gross National Product and one-third of total export revenues, with its share of the economy due to increase as production, and possibly oil prices, rise (see Table 9.1). In addition, the offshore supplies industry plays an important economic, political, cultural, and social role in Norway's regions.

Norway's petroleum sector will play a vital part in Norwegian economic and foreign policy making as Norwegian petroleum grows more important domestically and internationally. Two challenges in particular face Norwegian policy makers. The first challenge is to avoid following other petroleum producing nations (such as the Netherlands and Venezuela) that have failed to derive sufficient long-term economic benefits from the petroleum sector. The second challenge is to conduct a foreign policy that avoids entanglement in the frequent international conflicts that involve oil.

This chapter examines the

role

of oil and gas in Norway's domestic economy and foreign policy. First,

it looks at the development of the Norwegian petroleum sector since the

1960s. Second, it discusses how Norway has tackled the economic and

political

challenge of being an "oil nation" from a macroeconomic and foreign

policy

perspective. Third, it explores the place of Norwegian gas in a

changing

Europe. And finally, the chapter looks at how the EC's new internal

market

may affect Norwegian petroleum policies.

EXPLORATION, DEVELOPMENT AND PRODUCTION

Applications for exploration on the Norwegian continental shelf were made as early as 1962 and 1963 by international oil companies. Drilling started in 1966 after Norwegian authorities established the necessary legal framework and conducted the first concession round. During the period 1966-71, international oil companies explored the southern parts of the continental shelf where Phillips Petroleum eventually discovered the giant Ekofisk field in December 1969, thus proving the sector's significance for Norway (see Figure 9.1).

Figure 9.1: "Geographical Distribution of Resources". Source: OED, Fact Sheet 1992, 75

The 1970s saw huge investment expenditures but only moderate income from the offshore sector. The first oil was shipped by boat from the Ekofisk platform in 1971, but Ekofisk did not really start its commercial life as the first major Norwegian field in production until the pipelines to Teesside, England (oil) and Emden, Germany (gas) came on stream in 1975 and 1977. In 1977, the Frigg gas field (61 percent Norwegian, 39 percent British) started supplying Britain through the twin pipeline to St.Fergus, Scotland, as well. The huge Statfjord field (85 percent Norwegian, 15 percent British), discovered in 1973, started oil production in 1979. The smaller Murchison oil field and Valhall oil and gas field close to the Ekofisk area started production in 1980. Thus, by 1980, combined oil and gas production reached 50 mtoe, approximately half oil and half gas (see Figure 9.2). This was not enough to really call Norway an internationally significant producer, but the country had developed a domestically important economic sector by overcoming major technological challenges to deep-water petroleum development.

Figure 9.2: Graph, Norwegian oil and GasProduction Source: OED, Fact Sheet 1992, 75

In the 1980s, Oil production more than tripled, making Norway one of the largest exporters in the world (see Figure 9.3). Increased production from the Statfjord field accounted for much of the early growth, while oil from nearby Gullfaks (1987) and Oseberg (1988) fields provided an end-of-decade boost. Further increases in the 1990s will come from the start-up of Heidrun, Draugen, and a number of other smaller fields, as well as additional Gullfaks and Oseberg production.

Gas production, on the other hand, has remained at approximately the level reached in 1980. The Sleipner and giant Troll fields are expected to increase production dramatically when they begin producing in 1993 and 1996, respectively. This gas will flow to the European continent through the new Zeepipe (to Zeebrügge, Belgium) and Europipe (to Emden, Germany) pipelines. Norway is under contract to supply 40-45 BCM from these fields to replace gas from many of the older fields being phased out under field depletion contracts. Pipeline capacity, however, will stand at 60-70 BCM making it possible for Norwegian gas exports to pass 50 BCM within a decade and raising the country's annual oil and gas production to 150-200 mtoe. While oil accounted for all the increase in petroleum production in the 1980s, increases will to a larger extent come from growth in natural gas production in the 1990s (see Figure 9.2).

Figure 9.3: Norwegian Oil in the World Market Source: OED, Fact Sheet 1992, 75 Production Net Exports

Petroleum production has, until now, taken place in the North Sea south of the 62nd parallel but will soon move north. Development has already expanded north to Haltenbanken (off mid-Norway) where the Draugen and Heidrun fields are located (see Figure 9.4). A planned methanol factory at Tjeldbergodden will become the first domestic gas user by taking associated gas from these fields. Further north, oil companies have proven large gas reserves in the Barents Sea. Long distances to markets (2000 km to the Continent), environmental concerns, production costs, and market prices indicate that production may not start there for a decade or two. This gas, if and when produced, will most likely be transported by tanker as Liquified Natural Gas, thus opening up the possibility of gaining new customers in Southern Europe and the United States. For oil, however, transportation costs are lower, so northern production may commence more quickly if large recoverable reserves are found.

Figure 9.4: The Norwegian Continental Shelf

The area furthest north and east in the Barents Sea, which shares a border with Russia, has not been fully explored. Geologists expect it to contain significant amounts of petroleum, in part because the Russians have already proven both oil and gas east in the Barents Sea. A dispute between Norway and the former Soviet Union has precluded exploration in this area. The disputed area is larger than the entire Norwegian sector south of the 62nd parallel. Norway bases it claims on a mid-line principle, while the former Soviet Union based its claims on a sectorial principle. Fisheries, the territory's tremendous potential as a petroleum province and its military sensitivity make the border issue especially difficult. In addition, the huge military complex on the Kola peninsula and the narrow channels to the Atlantic Ocean for Russian warships and submarines presents a unique security problem for offshore developers. Plans are made to proceed with the negotiations between Norway and the new Russian leaders in near future. The Jeltsin government's attitude towards the dispute with Japan over the Antilles may, however, indicate that the controversy with Norway in the Barents Sea may not be easier solved than before, either, and it may still take a lot of time.

On the regional level, the counties around the "oil towns" Stavanger (Rogaland), Oslo (Oslo/Akershus) and Bergen (Hordaland) have increasingly become more important. In spite of the fact that activities on the shelf has been more spread (to the north) over time, employment has been more concentrated. In the period 1981-89, the three counties increased employment in this sector with 16.000 people, while the rest of Norway reduced employment with 6.500 people, secondary and derived activity included. The most concentrated activity is in Rogaland, covering some 50 % of overall employment in the sector.

PETROLEUM AND NORWEGIAN MACROECONOMICS

The Norwegian government made it clear from the beginning that it would play a strong role in the development of the petroleum sector. The nationalization of multinational companies in Arab countries before and during the first oil shock in 1973/74 made significant state participation politically acceptable in the 1970s. In Norway, two important objectives helped guide government policy. First, as much of the economic rent from the petroleum sector as possible was to stay in Norway to benefit "all Norwegians." This was possible because the Government had the property rights to the resources. Second, oil companies operating on the continental shelf were to prefer Norwegian offshore suppliers if otherwise competitive with foreign companies. To meet these objectives, the government also gave support to some larger industrial projects. In addition, the Storting, in 1972, created Statoil, a 100 percent state-owned oil company, that Norwegian authorities decided should have at least 50 percent ownership in new licenses. The Storting also established the Norwegian Petroleum Directorate (1972) and the Ministry of Petroleum and Energy (1978), and devised a special tax system for the petroleum sector (1975).

When world economic growth declined after the first oil shock, the petroleum sector allowed the Norwegian government to pursue an economic policy designed to counteract the downward trend, then expected to be temporary. In 1975-77/78, the "Kleppe packages" (named after the secretary of the Treasury) maintained domestic demand and subsidized traditional industries by borrowing abroad in the (correct) anticipation of high future oil revenues. These expansive budgets, together with high investments in the petroleum sector, raised domestic prices and made it difficult for new industries to compete. The program kept alive traditional and, what later turned out to be, less competitive industries by drawing resources from the rest of the economy. Even though Norwegian economists were well aware of problems like the "Dutch disease," many mistakes made by other countries with (expected) windfall petroleum profits were repeated.

The tripling of oil prices in 1979/80, higher production volumes, a strong dollar, and a taxation system that funnelled much of the economic rent to the government resulted in an "oil bonanza" in Norway. After a few years of contractive budgets following the Kleppe packages, public spending expanded again after the second oil shock while world economic growth levelled out. Domestic prices rose and the Norwegian kroner appreciated as a result of the oil-fueled trade surpluses. Once again, many industries competing with foreign firms domestically or internationally were priced out of their markets. Norway became even more dependent than under Kleppe on high (and volatile) oil revenues. In the period 1977-84 as much as 6 devaluations (varying between 2% and 8 %) of the Norwegian kroner was made to mitigate the problem. But the structure of the economy remained to a large extent unadjusted to the new international surroundings.

The seriousness of Norway's economic situation was made politically clear when oil prices dropped in 1986. A trade surplus of NOK 30 billion in 1985 became a deficit of NOK 20 billion in 1986 by the change in price of this single commodity. The petroleum sector's share of Gross Domestic Product fell from almost 20 percent to less than 10 percent (see Table 9.1). The liberal coalition government of Kåre Willoch, in power during the bonanza years, had to give the reigns of government back to the Labor party and Gro Harlem Brundtland after failing to pass a proposal of excise taxes on gasoline. The Brundtland government devalued the Norwegian kroner with 12 per cent and started to cut public spending. The second half of the 1980s were characterized by low oil prices, an unstable parliamentary situation, a gradual lowering of inflation, higher unemployment rates (by Norwegian standards), and high interest rates that protected the currency against devaluation, but also lowered investment. These elements combined to restrain growth in the Norwegian non-oil economy.

In the early 1990s, Norwegian oil revenues started to increase again, mostly due to higher production volumes. Budgets have become more expansive, but people have to a large extent used higher wages to pay back loans from the "happy" 1980s instead of increasing domestic demand. Economic activity is still relatively low, while unemployment was at the highest level since the Second World War (some 8% of total employment force in 1992). The petroleum sector itself is too small to reduce unemployment significantly. It is characterized by low labor and high capital intensity. Employment in the sector represent less than 1 % of overall Norwegian employment as the primary part is concerned (see table 9.1) and 2-3 % if it's secondary and derived activities are included. Furthermore, much of this labor requires special skills and higher education. Many foreigners are still employed (and needed) in the sector, even though the number of foreigners have declined in line with competence build up in Norway.

Most politicians wish to

avoid

repeating the economic policy mistakes of 1975-85, but no government

has

implemented a plan to transform (potential) windfall profits in the

petroleum

sector into internationally competitive non-oil industries (competitive

with EC countries and the new fast-growing economies in Asia) or

overseas

investments that could stabilize offshore revenues (following the

Kuwait

model). These are typical economic policy problems for oil and gas

producers

that to a large extent have remained unsolved in Norway as well as

elsewhere.

However, the financial situation of the Norwegian Government with

respect

to future petroleum revenues seems rather solid. Norway's petroleum

asset

was in 1992 calculated to 710 bill. NOK (1992-value) of which the

Government

share represented 580 bill. NOK (1992-value). Nevertheless, the value

of

this asset depends largely on the volatile price of crude oil.

A

break-down of the oil market could turn this positive part of the

economic

picture to another negative one.

NORWEGIAN ENERGY AND FOREIGN POLICY

Norwegian international petroleum policy is formulated at the intersection of national economic considerations, petroleum resource assessments, offshore project economics, regional and foreign policy goals. From both a revenue and cost perspective, Norway desires a "reasonably" high price for oil, or a highest possible value of the petroleum asset. At the same time, Norway is historically, culturally, economically, and politically part of the oil-consuming Western world. The West's desire for security of supply corresponds with Norway's interest in stable customers. The stability and predictability are considerations most consuming and producing countries have in common and, therefore, do not usually possess any large potential for. But the Western world, in direct contrast with Norwegian interests, is best served by high and stable production at "reasonably" low prices. Norway, of course, is not well served by prices so high that its Western trading partners suffer serious economic decline. High oil prices may actually damage Norwegian economy by making it more dependent on oil (an thus more vulnerable to price instability) and, perhaps, by offsetting gains from the oil sector with severe losses in other Norwegian exporting sectors. Similarly, too low prices may damage consuming countries interests as high cost production outside the Middle East will be reduced and, thus, increase the West's dependency on these politically volatile sources. Norway's associated membership in the International Energy Agency (IEA) is an expression of these diverging interests with the other Western countries.

Norway will attract attention from countries dependent on oil and energy markets developments, whether in OPEC or the IEA. The IEA will naturally stress to Norway the need for secure supplies and moderate prices in a tight market where prices are rising. In a weak market, other oil-producing countries will probably place pressure on Norway to limit supply to support prices, like they did during the OPEC-Norway "dispute" in 1985-86. Thus, in any status of market, Norway is likely to feel pressure from countries with diverging economic interests.

Up to May 1986, official Norwegian international oil policy followed what was called a "purely commercial line"--that is, Norwegian officials were not willing to admit that political considerations affected policy. The best policy was not to have one. Norway was in a good position as a "free rider" in the oil market; production could increase while the country benefitted from OPEC production reductions. In this fashion, Norway could maintain that petroleum policy was formed solely on commercial grounds.

However, contrary to the official Norwegian position, other countries were affecting Norwegian oil policies by the beginning of the 1980s. The sale of oil to Israel in 1982, the British rejection of the Sleipner Agreement (a gas contract) in 1984, and the "oil-option policy" (favoring oil over gas production), which was inspired by Norway's inability to sell high-priced gas on the Continent, were all influenced by political and strategic thinking. As the decade wore on, it became gradually more difficult to follow a "pure commercial line," in part, because OPEC considered Norway and other non-OPEC producers important players in the oil market. During the last two months of 1986, the Norwegian government, in a gesture of support for OPEC, withdrew 80,000 b/d from the market. In January 1987, it decided to reduce production by 7.5 percent in relation to production capacity. In 1990, the government dropped this restriction as the oil market gradually tightened. Norwegian authorities officially called the production restrictions unilateral, but in reality--since they were made conditional on certain policies pursued by OPEC--were the manifestation of Norway's bilateral relationship with the organization.

The natural gas market in Europe, for several reasons, tends to be even more politicized than the global oil market, even though gas prices has been (indirectly) linked to the price of oil. First, European gas has crossed important political, cultural, and economic borders for several decades. The main exporters are non-EC-members Russia, Algeria, and Norway and EC-member the Netherlands. Consumption takes place largely within the EC. Central and Eastern Europe has until now been supplied only from Russia, illustrating their economic and political dependency on the former Soviet Union since the Second World War. Second, gas trade rigidly links producers and consumers to each other through expensive pipelines. Trading countries are highly interdependent because large economies of scale in production and transmission make feasible long-term contracts involving enormous volumes of gas and huge sums of money (both in construction work and gas contracts). Third, gas trade involves security policy, as illustrated by the United States' 1982 embargo on equipment for a new Soviet pipeline. Finally, success in the European gas market, more than in most other markets, requires an ability to 1) utilize existing political ties and rules of trade to your advantage and 2) establish new political alliances and trading rules when necessary. Even a marginal change in business terms will soon affect the distribution of great sums of money between contracting parties.

Norwegian governments have long attempted to make gas trade (like oil trade) "nonpolitical." In 1986, however, the French government, before it would sign a contract for Troll gas, required Norway to agree to a series of measures unrelated to the gas trade that would increase economic, political, industrial, cultural, and scientific cooperation between the two countries. After a period of intense diplomacy, Norway accepted some of the French requirements. Thus, after Norway supported OPEC's efforts to stabilize the oil market and signed the Troll deal with France, both in 1986, Norwegian authorities declared that Norwegian petroleum policies was influenced by foreign policy considerations, not just commercial principles.

NORWEGIAN PETROLEUM IN A CHANGING EUROPE

The process of economic and political change, both in the EC and in the East-West context, is affecting the field of energy. Growing economies, increased environmental concerns, a desire to reduce dependency on Middle East oil, and the need for new gas sources to balance increased gas imports from Siberia indicate a need for more Norwegian natural gas. Since Norway, unlike its European neighbors, is a major energy exporter (and likely to be one longer than any other European exporter, except Russia), its participation in the making of future EC energy policy may prove to be vitally important to Norwegian energy interests, regardless of Norway's formal relationship with the Community.

The changes in Europe may carry less significance for Norwegian oil than for natural gas. Oil is an internationally traded commodity that is transported around the globe and sold to anybody (barring political obstacles) at world market prices. Economic and political processes in Europe will generally have less influence on the price of oil than, for instance, the situation in the Middle East, United States oil policy, and the global demand for oil. Nevertheless, in tight market situations and periods of international instability, Norwegian oil contribute to reducing the possibility of another oil shock and may notably influence prices. Thus, under certain circumstances, Norwegian oil does play a role in the security of supplies for importing European countries. In this role, Norway is perhaps more important for consuming countries and the EC than the EC is for Norway.

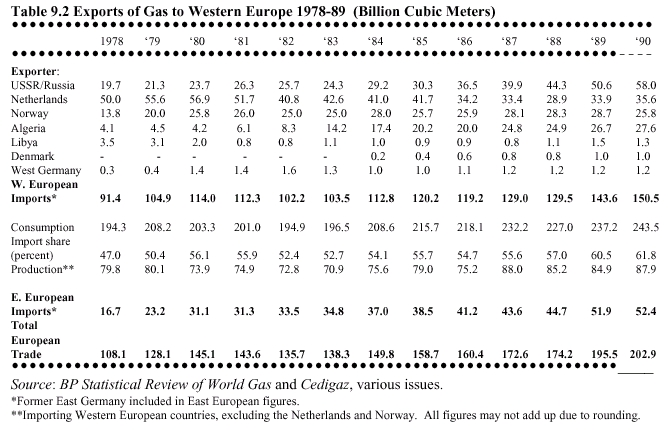

The future structure of the market for natural gas, with its expensive infrastructure and strong, long-term interdependence between buyer and seller, will be extremely important for the development of Norwegian gas export revenues. Today, the European Community purchases 100 percent of Norwegian gas exports, and Norwegian gas represents 20 percent of Western European gas imports (see Table 9.2). Access to pipelines, pipeline tariffs, market prices, the availability of gas to end-users, and EC fiscal policies all affect Norwegian gas sales.

When considering the gas market, the EC Commission has focused on the concentration of power over the export, import, and transmission of natural gas. It considers the market to be dominated by monopolies:

If an industry is not structured to operate competitively, some sort of state intervention is normally needed to reduce the social losses incurred by the monopolistic and/or monopsonistic behavior of the companies involved. Such behavior does not usually lead to the most cost-effective way of producing a commodity or service since large gaps are often left between price and cost. Both seller and buyer of the pipeline service, as well as the pipeline itself, wish to capture the net benefit, thus each may have a different view of how the market should be organized, which again may differ from society's view. The regulatory complexity, as experienced in the United States, and the conflict of interests explain why regulating pipelines is always a complex and controversial economic and political issue.

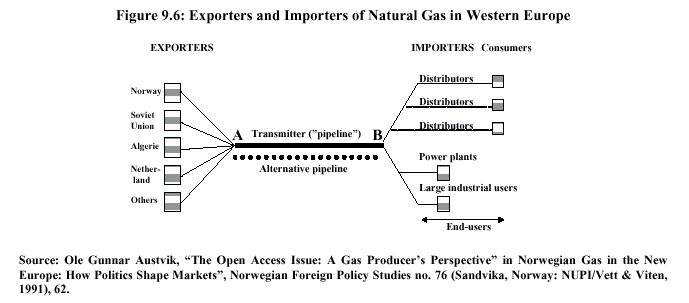

In Europe today, gas exporters sell their gas to the major pipelines. The pipelines transport the gas and sell it in the "end-user" markets. Many of the pipeline companies are organized in purchasing consortiums, but the suppliers (e.g., Norway, Russia, and Algeria) do not cooperate. Some competition among suppliers and distributors, and its absence among pipelines, may have caused exporters to ask lower prices, importers to pay higher prices, and pipeline companies to receive higher profits than might otherwise have been the case. Since pipelines tend to be natural monopolies for technical and economic reasons, their cooperation makes for a very concentrated market structure, underlining the strong position of the transmission lines in Europe.

Under an open access regime, the exporters will sell their gas at point B (see Figure 9.5) rather than at point A. But, will the old monopoly structure then be replaced by a new one consisting of producers and importing firms? And what about prices at different stages in the market?

It seems unlikely under an open access regime that (oligopolistic) producers could manage to charge customers higher prices than (monopolistic) transmission lines do today. Whether the prices to end-users (in this context: distribution companies, power plants, and large industrial users) remain the same or decrease, will, to a large extent, depend on the positions of importers and exporters in the market. The stronger the position, the higher the potential for increased economic rent. Both parties wish to redistribute the possible economic profit of the pipelines to themselves. Therefore, it is logical for the Commission to consider regulating producers' and importers' monopolies.

As long as EC countries are mostly importers of gas, and the most important exporting countries are non-EC members, the regulation of a producers' oligopoly may prove difficult (although this may change somewhat if Norway becomes an EC member). Therefore, from the consuming countries' point of view, some sort of monopsony (or oligopsony) power should be maintained to balance possible producer market power. With a market structure like the one in Western Europe, the change may be marginal for many actors and it may lead to new inefficiencies in the market as income is redistributed from pipelines to producers and/or importers.

One argument against some sort of an open access solution is that it will challenge the long-term stability producers enjoy in today's contracts with the transmission lines. Today, transmission lines have take-or-pay obligations that secures investment on the Continental Shelf.

However, one reason why these contracts are long-term and stable is that consumers have a stable need for natural gas. It is difficult to see why this stability cannot be maintained when producers sign contracts with the customers directly rather than indirectly through the transmission lines. This being said, the transition itself will incur costs when moving from the existing system to a new one. Therefore, a gas producer may end up with a negative view of the proposal in the short term but a more positive one over the longer term.

As a start on the process, the Commission has introduced a "Transit Directive" to allow high pressure transmission lines access to other transmission networks, and is considering some sort of "Third Party Access" rules which, inter alia, shall allow importers and exporters similar rights.

Obviously, regulations and arrangements in this sector are economically, legally, and politically complex. For more than fifty years the United States has struggled with this issue in court, in legislatures, through regulation and deregulation. In Europe, we should similarly expect strong resistance to any regulatory efforts, especially from the pipelines.

The difficulty in settling issues--reasonable transportation rates, depreciation periods, whether all tariffs should be equalized or not, the allocation of excess demand, optimal pipeline capacity, and the pricing of new capacity--should not be underestimated. Therefore, we should not rule out alternatives to open access, such as increased competition (where it is possible), establishing publicly owned pipelines, anti-trust legislation, and taxes and subsidies.

The transition period to a new system may last for a long period with both old and a new rules, to various extent, functioning in the market simultaneously. In the field of natural gas, the single internal market is not necessarily introduced as a dramatic shift from one set of rules to another at the end of 1992. "Project 1992" also symbolizes a process that may last throughout the decade where various regulations and arrangements may be introduced on a flexible basis.

The companies operating on

the Norwegian continental shelf may hold diverging views on these

market

changes. If EC regulations are applied offshore in the future, the

expensive

pipelines now earning substantial profits may lose. Those companies

interested

in making money transporting rather than producing gas may oppose the

proposals

for a more open network. Some companies also argue that such

regulations

potentially lead to more, not less, bureaucracy and inefficiency.

EC SINGLE MARKET AND NORWEGIAN PETROLEUM POLICIES

In the 1970s and 1980s, expected and actual oil revenues contributed to the raising of domestic Norwegian prices and forced many "traditional" industries out of business. Some of these symptoms parallel the "Dutch Disease" experienced in the Netherlands after their natural gas exports began in the 1960s. If Norway again reaps windfall profits from the petroleum sector in the 1990s, similar problems may recur. The issue, however, can no longer be dealt with in the same way as in the 1980s. The Norwegian kroner is now linked to the ECU, making it much more difficult for the government to employ currency devaluation to mitigate problems caused by inflationary effects of oil revenues. Interest rates too must be harmonized with European levels to maintain a stable currency. Thus, the tieing of the kroner to the ECU has restrained the government's ability to use monetary policy instruments to affect the economy. The fact that the raw-material based Norwegian economy functions differently than the industry-based EC (and other Nordic countries) economies is a central dilemma on this issue.

In addition, an EEA agreement or a full EC membership will further limit the availability of traditional economic policy tools, by limiting the use of direct subsidies and transfers to industries about to go out of business. With only an EEA agreement, the availability of EC restructuring programs will also be difficult. Thus, the problems for Norwegian exports may become worse in the 1990s if inflation again exceeds European levels and the use of monetary policy instruments remains restricted. From the heavy economic dependence of Norway on the EC, fiscal policies could implicitly be harmonized with EC budgets, as well. Even though autonomy will be greater in fiscal than in monetary policies, the possibility of implementing much more expansive budgets than Norway's most important trading partners may become more difficult than before. Over time, the only way to be competitive in European markets is to keep costs down and improve efficiency. That may not be bad for the economy, as it implicitly may force a restructuring to take place. But the macroeconomic freedom of action, and, thus, the ability to implement comprehensive and independent national economic policies, may become further restricted. This situation stems first of all from the heavy dependence of Norwegian economy on the EC. Thus, with or without an EEA agreement or EC membership, Norway needs to find new ways to use oil revenues so that incomes will not produce undesired inflationary effects.

One approach is to create an oil fund. Such a fund was established in 1990 in order to separate oil taxes and royalties from other public revenues. However, this fund accrues all revenues from the petroleum sector and has not really changed the past practice of combining oil revenues with the rest of the budget. More or less it is only the name of the account that has been changed. The Storting can still use all of it to balance deficits, from the logic that the best democratic decisions for the country's economic future, anyway, is, by definition, made just there. The net present value of future revenues accrued in this fund correspond to the government's share of the calculated petroleum asset mentioned above. Norway can be rather sure to receive some of this calculated asset, for example those accrued even if prices drop down, let's say 10 $/bbl. However, the part of the calculated asset that is accrued from increasingly higher prices is more and more risky. Norway may get it, or not, depending on the volatile price of crude oil.

One alternative approach for the oil fund could be to place incomes that origins from oil prices above a certain level into it (for example 15-20 USD/bbl), while incomes that origins from prices below this level is accounted for in general budgets. Obviously, revenues that origins from the higher part of a price are potentially more unstable than revenues from the lower part as a high price is the sum of the lower and the higher part, while a low price only consist of the lower part. It is the "money shower" from this higher part, periodically received by Norway and other petroleum producers when oil markets fluctuate, that may be considered the main macroeconomic challenge as far as instability is concerned. After a period of high prices, prices may eventually drop down to the lower level again.

A fund of such volatile revenues should not be used to balance domestic budgets, but be invested abroad or at home in order to create earnings in foreign currency in the future. A policy of investing abroad has it's parallel in Kuwait's policy over the last couple of decades. Before Iraq's invasion in 1990, half of Kuwait's earnings in foreign currencies originated from such investments and contributed to stabilize their trade balances. If Norway chose a more outward-looking economic strategy in the future, a policy of domestic investments, could, in addition, be linked to the development of industries exporting to markets with higher international profits and growth rates than most Norwegian export industries sell in now, i.e. develop long run comparative advantages. Instead of giving direct support to certain industries, which easily may come into conflict with increasingly more comprehensive GATT-rules and the establishment of the EEA, support could be given to the development of infrastructure like roads, railway, air services, telecommunication, education and research. Obviously, the distinction between which part of these that should be covered in "normal" budgets as opposed to the other part that should be designed in a more or less temporarily fashion dependent on oil revenues should be clarified. Given this clarification, such investment and (fixed cost) support would lower costs in industry and improve efficiency and international competitiveness. If the desire is to support growth in specific sectors (as they do for example in Japan), general type of support should be given to areas which is important for the development to the specific selected sectors.

If, on the other hand, volatile petro-money is continuously used to balance domestic budgets, inflation rates -- and thus costs in non-oil industries -- may again rise higher than trading partners. Devaluation can only with the greatest difficulty be used to mitigate the problem, and it would, nevertheless, conserve the industrial structure, so the economy may remain in a stop-go pattern to a large extent following fluctuations in the oil market. A continuous reliance on an inward-looking economic strategy will require more protection from international competition for Norwegian firms. GATT-rules and (simultaneously) the establishment of free-trade blocs (such as the EEA) make it doubtful that Norwegian industry can acquire such protection. If tomorrow's industrial and trade policies are the same as yesterday's, the creation of new economic activities and jobs may prove to be very difficult. More likely, some old jobs will disappear without the replacement of new ones.

Norwegian international energy policy has balanced the various interests within the country against interests from abroad, such as those emanating from OPEC, the IEA, and others. European integration will make the body of the EC an additional important actor in this area. If trans-European gas networks, including those from Western Siberia, are subjected to EC regulations, the EC will become only more crucial to Norwegian energy interests, perhaps the most important one. Having the joint interest with consuming countries in stability and predictability in energy trade, and the huge flow of petroleum from Norway to the EC, there is an interdependence between the two on this issue. The conflicting economic interest may simply be considered as a question of distribution of economic rent between producer and consumer, i.e. the price of oil and gas, and in particular producer's price on gas. Norway wish to secure that arrangements are made that leaves a "reasonable" rent to the producer, constrained by the fact that prices should not be higher than that they permit economic growth in the EC and the rest of the world, to the benefit of Norwegian non-oil exports, as well. Of course, the EC's perception of what is "reasonable" may differ from Norway's. The overall economic and political relationship, positions and processes between and within Norway and the EC, as well as the tightness of petroleum markets, will decide which party will benefit the most from this interdependence. Actors within the Community (as well as other consumers and producers) have strong incentives to influence Norwegian policy-making on these issues. Obviously, Norway need to formulate independent policies, member of the EC or not, being aware that no EC country share her interest in the distribution of rent.

As the perhaps largest energy exporter in Europe, Norwegian policies will attract increasingly more attention from the rest of the world. This may give Norway new and improved relationships with other countries. Petroleum may increase influence in international politics and economics in general as well as on energy specific matters. On the other hand, the property rights to huge energy resources, and Norway's own dependence on revenues from the sector, may also turn world attention into pressure. Norway's large area, significant energy resources and small population parallel some of the characteristics that can be attached to Kuwait in the Middle East. Like Kuwait, in a possible political conflict which soon may involve the battle over the control of energy resources, Norway will obviously not be able to defend herself against aggression from larger countries alone, either the future aggressor comes from East, South or West. Obviously, today, for most people military aggression towards Norway may seem to be an extreme and rather unthinkable possibility. However, in a long term perspective, being attractive from both a territorial and energy perspective Norway have to choose alliances to protect herself. The membership in NATO has been one way of showing which side Norway will rely on in a conflict. But political pressure has many stages before the ultimate war and it should be an important policy objective to have a range of instruments and arrangements to prevent aggression on all stages and forms. A membership in the EC will link Norway stronger to the other Western countries through increased political and economic integration and, thus, improve Norway's security situation. But, obviously, Norway has to be aware that such a security link may also be used to push down producer's rent.

In the European gas market, one effect of the reregulation will eventually be that both exporters and importers must increase their commercial activity in the markets to replace the broker role of the transmission lines today. If so, producers should build a portfolio of direct customers, stabilize incomes, and possibly increase sales. End-users (in this context: distribution companies, power plants, and large industrial users) will allocate purchases between local producers and exporters to optimize their portfolio so as to secure supplies and minimize dependency on each seller.

A gas strategy that does not include such an increase in activity may run the risk of losing market share in the long run. The ability of the companies and the government to pursue an active market strategy while also influencing policy makers and regulators in Brussels may determine whether the net result of the changes in the gas market will be positive or negative for Norway. The final content of EC energy policies may remain uncertain for a number of years ahead. But the direction seems clear. Therefore, strategic investments, for example in pipelines and LDCs, should in certain situations be considered along with continuing the good relationship to the huge transmission companies. Furthermore, EC regulations that affect the way gas sales are organized could push down prices to the producer by establishing competition between gas sellers on the Norwegian shelf. Norwegian policy makers should concentrate on maintaining maximum bargaining strength versus the market, informally or formally, as before through the Norwegian Gas Negotiation Committee (GFU), or through the creation of new institutional arrangements. One much used argument has been that coordination of gas sales is necessary in order to be able to optimize the resource portfolio.

In the offshore supplying sector the EEA agreement assumes that foreign firms will be given the same competitive status as Norwegian firms. The elimination of offshore discrimination and "public procurement" may reduce costs to the benefit of the oil companies and the government take, but to the detriment of Norwegian supply industries. However, the principle of reciprocity demands that Norwegian firms will get easier access to the British and other countries' offshore sectors. The size of these other markets, the proximity of Norwegian firms to Britain, and the high level of competence in Norway in this area indicate a potential for market penetration. The potential losses in the home market may be balanced by gains in other offshore markets and the comparative advantage that Norway has developed in this area may be further exploited. With the concentration tendencies of the employment around Stavanger, Bergen and Oslo that has taken place as the sector has become more mature, indicate that these areas will benefit the most from participation in the Single market in this sector on the regional level.

If Statoil in the long run cannot be used as a petro-political instrument to the same extent as before, the government may have to strengthen the Ministry of Oil and Energy's position in relation to the companies in order to take care of Norwegian interests. This may also be necessary if concession rules are changed into a non-discriminatory fashion. The proposes concession directive is, however, not a part of the present EEA agreement.

As a start on the process, the Commission has introduced a "Transit Directive" to allow high pressure transmission lines access to other transmission networks, and is considering some sort of "Third Party Access" rules which, inter alia, shall allow importers and exporters similar rights.

Furthermore, environmental arguments may be used by the EC to increase petroleum taxes, even though the actual reasons are to take rent and power from oil producers (OPEC) and reduce consumption of imported fossil fuels. Norwegian economic interests will be harmed by this. Until now, Norway has pursued a rather strong voice on environmental issues internationally. In the future Norway may emphasize foreign policy in this area more in the direction of defending her economic interests (shared by no other EEA country) rather than her environmental interests (shared by many other countries), much in the same way OPEC countries already argue today. If Norway, the major petroleum exporter in Western Europe, changes the emphasis in her foreign policy to favor energy over the environment, and becomes a member of the EC, EC environmental policy debates may be influenced in a new way.

From an energy perspective, would Norway be better off as a member of the EC? The evidence is mixed. From a security political point of view the answer seems to be "yes". An overall stable and foreseeable security situation may also promote investments and economic growth. Norway should, however, avoid that a tighter political link to the Western countries is used by Norwegian allies to press producer's prices down. Furthermore, with a membership, EC regulations will more directly affect Norway. In the field of energy, the country may have a say in these dynamic processes also as a non-member, even though its voice would, probably, be louder if she had a member's seat at the table. But as long as no EC members share Norwegian interests in the distribution of economic rent in energy trade, Norway will have to pursue a more independent commercial and foreign policy in this area, than just adapting to general EC policies. Thus, the overall question of membership should, perhaps, from an economic point of view, be decided upon on the basis of other factors important to the country. For energy, because of Norway's mixed interests, it seems that it first of all is the ability and will to dynamically influence and interact with decisionmakers in Brussels that is important along with the ability to create a dynamic attitude that reaps the benefits and avoids the problems of the new international surroundings.

ENDNOTES

. All Statfjord oil is shipped by boat from the field. Statfjord gas production started in 1985 with the opening of a pipeline system.

. The disputed territory covers 160,000 km2, 20,000 km2 larger than the North Sea sector, which covers an area approximately the size of Colorado.

. The primary oil activity comprises employment in oil companies, drilling, service and supplies industries. The secondary activity includes industrial construction activity. The derived activity covers the build-up and running of refineries and terminals. See Odd Einar Olsen and Jan Einar Reiersen, “Svart gull på alles fat?” Oljevirksomhetens regionale fordeling”, Kommuneforlaget, 19991.

. However, the devaluation was made in a situation of full employment. This may have contributed to higher inflation rates the following years than what otherwise would have been the case.

. The petroleum asset correspond to the net present value of future sales revenues minus fixed and variable costs in production and transportation. Government share is the net cash flow from the sector; taxes, dividends from Statoil and net payments from the central governments direct particpation in petroleum activities (SDØE). Obviously, it is difficult to calculate the value of this asset, as it depend on the development of the size of the reserves, technology, prices and the choice of discount rate. In the calculation made in 1992, oil prices are expected to remain at 120-126 NOK/bbl (some 20 $/bbl with a currency rate of approximately 6 NOK/USD), total reserves around 7.8 bill tons of oil equivalents and the discount rate chosen is 7 per cent. Source: Revidert nasjonalbudsjett 1992.

. See Norwegian Oil and Foreign Policy, ed. Ole Gunnar Austvik, Norwegian Foreign Policy Studies No. 68 (Sandvika, Norway: NUPI/Vett & Viten, 1989) for discussions on the formation of Norwegian oil-market policy and Norway's relations with OPEC.

. Bruce W. Jentleson, Pipeline Politics: The Complex Political Economy of East-West Energy Trade (Ithaca, NY: Cornell University Press, 1986) discusses this case in depth. Ole Gunnar Austvik, "Norwegian Gas in an International Context: The U.S. Embargo of Soviet Gas in 1982" in Norwegian Gas in the New Europe, ed. Ole Gunnar Austvik, Norwegian Foreign Policy Studies No. 76 (Sandvika, Norway: NUPI/Vett & Viten, 1991) discusses the Norwegian response to pressure to replace Soviet gas by increasing gas production.

. Commission of the European Community, "The Internal Energy Market," Working Document, 2 May 1988.

. The Commission of the European Community, "The Need for Greater Integration of Europe's Gas Grid," Energy in Europe No. 10, 1988.

. The pipelines themselves will, of course, suffer under such a regime. Much of the point of the regulations considered is to remove profits and power from the pipelines.

. Take-or-pay means that if the purchaser cannot use the gas contracted, he has, anyway, to pay for the contracted volume.

. See Jonathan Stern, "Third Party Access in European Gas Industries. Regulation-driven or Market-led", the Royal Institute of International Affairs, London, October 1992 for an overview of the steps taken by the commission on this issue.

. A more thorough discussion of the regulation of the EC market for natural gas is given in Ole Gunnar Austvik, "Europe 1992: Introduction of Common Carriage for Natural Gas?," Discussion Paper M-90-01, Energy & Environmental Policy Center, John F. Kennedy School of Government, Harvard University, 1990. Norwegian Gas in the New Europe presents a broader discussion of the role of Norwegian gas in the new Europe.

. The elimination of exchange rate policy as a tool of macroeconomic management has caused some economists and politicians to criticize the ECU link. See for example Fredrik Carlsens discussion in "Bør petroleumsfondet grunnlovfestes?", Norsk økonomisk tidsskrift nr. 2, 1992.

. For a discussion of the distinction between "stable" and "unstable" parts of the price of oil see Ole Gunnar Austvik, "Limits to Oil Pricing. Scenario Planning as a Device to Understand Oil Price Developments" in Energy Policy, London, November 1992. In this article, the long term development of the price of oil, given certain assumptions, is expected to lay on or between an upper (illustrated as 30-40 $/bbl) and lower (illustrated as 15-20 $/bbl) limit. Alternatively to financing the fund by the most volatile part of the price, the economic rent from the sector could be put into the fund. But the size of this rent is difficult to determine and it varies strongly between fields. Furthermore, it is not necessarily all the rent that is unstable and, thus, creates a problem.

. The GFU (headed by Statoil) is responsible for selling all of Norway's offshore gas. Alternative new ways of organizing gas sales are discussed by the President of Statoil's natural gas division in Terje Vareberg, "Major Challenges Facing Norway as a Gas Producer" in Norwegian Gas in the New Europe.