|

Gas Pricing in a Liberalized

European Market;

Energy

Policy, vol 20/no.12 pp. 997-1012. December

1997, London,

Download the article as pdf-file here Download the article from publisher here. |

Keywords: Natural Gas; European Union; Liberalization; Taxation.

Remark:

Many documents are linked up

in full text here. You are welcome to download and print them. Please,

be aware that inaccuracies may occur in some versions. Proper reference

to author, title and publisher must be made if you use the material in

your own writings, being in your organization or in public. However, the

documents cannot, partially or fully, be used for commercial purposes without

a written permit.

In the highly concentrated structure of the European gas market, gas is sold and resold many times on its way from the field of production to the final user, often between monopolies/oligopolies and monopsonies/oligopsonies. Generally, producers (exporters) sell gas to transmission companies (pipelines) who act both as transporters and merchants in the market. The gas the pipelines buy at it's entry, they resell at its exit at the city-gate to their customers; local distribution companies (LDCs), power plants and large industrial users. The LDCs act as both transporters and merchants, as pipelines do, and resell the gas to final consumers (end-users) in private households and businesses. Power plants and large industries are end-users themselves, and use gas as input factor in production processes, such as for electricity, chemical products etc. In general, producers and pipelines write long term contracts (up to 20 years), while pipelines write medium term contracts with its customers (1-5 years).

Prices for consumers are generally set in relation to the prices of the alternatives to gas for each consuming group. The highest gas prices can be found in households and businesses (the markets for the LDCs), the lowest for gas used in electricity production. Prices for producers are in contracts net-backed from consumer prices, with the withdrawal of margins to LDCs and pipelines, respectively. These margins are mostly based on capital costs and negotiation strength, and are independent on the market price of gas. Thus, producer prices vary with consumer prices, while gross margins to LDCs and pipelines do not. For gas to penetrate European energy markets, consumer prices in some contracts are set below the price of its alternatives.

As the European gas market becomes liberalized, gas need not be sold and resold quite so many times as under today's system. Under a completely and perfectly liberalized market system, producers should make direct contracts with LDCs, power plants and the industry, and buy transmission services from the pipelines (as for a toll road). The fee for this transportation should cover pipelines' normal profit, but should not give any economic profit to them. Pipelines' roles as both transporters and merchants should be unbundled, and they should act only as transporters. Intermediates, such as brokers and marketers, may become new actors to clear (parts of) the market.

While pipelines are often natural monopolies (or at best natural oligopolies) their behaviour and pricing practices should be regulated by a public authority. Producers and customers however, are not necessarily natural monopolies. In order to create competition in these segments, sales monopolies in exporting countries should be abolished, and customers should compete for gas (as they to some extent already do in today's market). Since LDCs are natural monopolies in the areas in which they operate (not their merchant function, though) it is necessary to regulate them as well. If the market theoretically is completely and perfectely liberalized, each firm in the gas chain either operates as a price taker, due to perfect competition, or is efficiently regulated by a public authority.

In the first half of this article, the process towards a more liberal Eureopan gas market is discussed. What are the objectives, forces and obstacles leading to a more liberal market? The main structure of how gas prices are determined in continental Europe today is described. Under various assumptions of how the market is liberalized, it is analyzed how prices may be affected. The question is raised whether the U.S. liberalization experiences are of any relevance for Europe. The second half of the article discusses the role of energy taxation in general, and gas taxation, in particular. The sharp increases in oil product taxation over the last decade, which has lead to assymetry in the devlopment of consumer and producer prices, is discussed, and the existing level of gas taxation is presented. It is analyzed how increased taxation on gas affect gas prices in todays market, and when the market gradually becomes more "liberal", respectively. Finally, the article argues that a more active use of gas taxation by EU governments makes a political-led liberalization process more attractive. However, the increased uncertainty caused by liberalization and the potential of higher gas taxes, may result in less new gas to the market, especially from new mega fields.

Competition versus regulation

For the functioning of natural gas markets, the most crucial element is the cost of, and access to, transportation. Cost of gas transportation is often characterized by strong elements of scale and scope economics, making transporting firms natural monopolies in the markets in which they operate. This situation exists within other types of communication as well, such as roads, harbours, airports, railways, mail services, telecommunications and public transport, within water- and electricity supplies, health services, education, cable-TV and garbage collection.

In Europe, many public utilities operating as natural monopolies were nationalized in the aftermath of World War II. Under nationalization, the management of a single firm should take care of both private and social goals. However, these monopolies were gradually accused of being slow to upgrade technology, service and productivity. Being monopolists by nature (but sometimes only by law), they were considered bottle-necks in the development of each nation's competitiveness. Probably, the most frequently used argument explaining these firms' inefficient use of resources, has been the lack of competition.

Liberalization of a such markets represents a departure from the "one management" approach. However, the particular aspect of by-nature non-competitive markets, is that the goals of competition cannot be achieved only by removal of trade barriers. If the most efficient operation of a market is done by one, or only a few, firms, these must be made to behave in a way that improves efficiency. This argument goes for product extension through vertical (or horizontal) integration and the exploitation of economies of scope, as well. In fact, an increase in the number of actors in such markets, per se, may increase cost, and, thus, represent a waste of resources. Indeed, removal of barriers of entry into the market, may not bring new firms into operation, necessarily. Usually, under liberalization, national owned firms are privatized (even though the government may hold a significant share or, or control over, the ownership), the operation of vertically integrated services are separated ("unbundled"). Competition should be established when possible, regulation when necessary (when competition does not work) and unbundling introduced when economies of scope are not present (or exhausted).

There are several factors determining pipelines' market power in addition to the scale and scope economies. One such factor is the power of producers and customers, respectively, that the pipeline meets at its end. By concentrating sellers and buyers power, a counterforce to mitigate pipelines' market power is created. In the European gas market, this is, to some extent, done at the supply side, which can be characterized more as oligopolistic than competitive. There are only a few exporting nations, and within each of these nations gas sales are orchestrated through one body. At the customers side, however, it is more difficult to concentrate purchasing power. Customers are placed in several consuming countries and there are many LDCs, power plants and industrial users within each of them. However, LDCs serving large urban areas may have a certain degree of market power, if it has (potential for) access to alternative routes of transmission.

In order to exploit economies of scope, producers have good reasons to integrate wholly or partially with transmission activities. In the Norwegian North Sea, this is done by giving producing firms property rights in off-shore pipelines. In Russia and Algeria, it is (so far) done by centralized firm(s) in Moscow and Alger, planning production and transmission to the respective countries' borders. This product extension contributes in realizing the oligopolistic market structure on the supply side. In the market, the long term contracts between producers and pipelines (in consuming countries), may also be considered as an approach to optimizing the advantages of joint management of transmission and production. Integration between LDCs and pipelines can also be argued for one the same base, even though it seems to happen to a lesser extent. Probably, this is due to greater dissimilarities between the transmission and retailing business, than between producing and transmission. Perhaps, integration between these is restrained by diseconomies of scope, reinforcing the impression of a more competitive structure across customers.

Even if it is not cost-saving advantages in bundling all kind of services, firms may nevertheless profit by doing so due to the benefits of increased market power. For a transmitter, for example, there may be economies of scale in transportation of gas but not necessarily economies of scope in the role as a wholesaler. The broker role may in some cases inhibit elements of economies of scope with the transmission service and in other situations it could be done more efficiently by independent firms. By having the exclusive rights (natural monopoly) in the transmission function, the pipeline company has the power to prohibit other companies wanting to act as brokers, take over their potential profit and obtain a monopoly in providing merchant service, as well. This will contain the contact between producers and end-users and decrease market efficiency. While the pipeline gains, there is a net loss for society.

The question is how large are the benefits of vertical integration and co-ordination are. The existence of scope advantages indicate that a liberalization of the market should open for the possibility to bundle services in competition with provision of unbundled services. The smaller the market and number of players, the less cost arguments seem to be in favour of unbundling operations. If operations are unbundled and there exists economies of scope, the gain from increased competition should be weighed against the losses of less efficient operations of each firm. Thus, with the growth in the European market, gradually more arguments support the idea of unbundling. When competition gradually intensifies, as, for example, seen by Wingas's entry into the German market challenging Ruhrgas, this part of the liberalization process could speed up.

In end-user markets, competition from other fuels, in particular oil products, but also coal and nuclear electricity, provide a price cap on gas. The prices of alternative energies represent the limit on total market turnover, and on how much rent the various segments in the gas chain can "fight over". If the shares that are distributed to transmission and distribution companies, continue to be rather insensitive to changes in end-user prices, changes in end-user prices will, in general and eventually, be to the loss or benefit of the producer.

Taken together, with some modifications, the barriers to entry is significant in pipeline transportation. Transmission companies have great potential of exercising market power both towards producers and towards customers. The potential for and benefits of market power, may lead to "over-bundling" of services and over-investment in capacity in order to deter newcomers.

The problem for policy makers is that a concentrated market structure may also be the socially most efficient one. The challenge is to intervene in a way that preserves a market structure that has the potential to minimize cost, but at the same time avoids possible lax cost control and exploitation of market power, following the strong position of the firm.

When competition and/or unbundling is impossible or inefficient, due to specific economies of scale and scope characteristics in firms costs and the market structures, a regulatory mechanism must be established to make the firm behave as if competition existed (by force or by incentives). In replacement for the "invisible hand" in the market place, a "visible" hand should be introduced, to use Adam Smith's terminology. This visible hand could be some sort of a regulatory authority, to define and oversee that the optimal combination of competition and regulation exists, and that it works according to its premises.

Towards a more liberal European gas market

Even though there have been elements of public policies towards production rights, the building of pipelines and operation of LDCs in Europe, there has been little interference into the trade of gas between producers and pipelines. This is partly due to the fact that European gas trade is international and must be dealt with on a bilateral basis. Sometimes, and especially between former Soviet Union and the former Eastern European countries and Finland, gas trade has been part of larger barter deals. There have also been examples on governmental interference in preventing contracts from, or promoting contracts to, being signed or fulfilled. Among such examples are the U.S. embargo of equipment to the Soviet pipeline, the French subsidization of Algerian gas import and the British rejection of the Norwegian Sleipner contract, all in the 1980s.

Both market growth and infrastructural developments, as well as political decision making, may now create a more competitive gas market. Competition between pipelines will most likely intensify. Market growth indicates that competition between customers may intensify. Increased demand may bring new supplying countries to the market, such as Kazakstan, Iran and others, and increase the number of oligopolists selling to the market.

Hard competition between producing companies within exporting countries is less likely to be allowed by exporting countries themselves, due to the desire to sustain market power and exploit economies of scope in production and transmission (within the exporting countries), as well as of general resource management needs. This has been an argument against liberalization of the market. From consuming countries point of view, the maintenance of an oligopolistic supply side while the market is liberalized downstream, may give sellers a disproportionate market power and potentially enforce an anti-competitive situation. Thus, there is a desire, from EU point of view, to weaken or dissolve gas exporting countries sales monopolies. From the producing countries point of view, the loss of long term contracts with the pipelines, will distort investment incitements. Thus, either part may be prevented from introducing more competition in its gas industry if a neighboring country does not, for fear of causing a relocation of rent.

Although it seems likely that the European gas market will become more liberal than it has been, there are many reasons why the European gas market will not become completely and perfectly liberalized in the foreseeable future. Firstly, the varying degree of scale and scope economies in market segments, makes it difficult to establish an optimal portfolio of competition, regulation and unbundling throughout any gas chain. It is also difficult technically to find regulatory schedules that do not create new inefficiencies in the market. The second-best solutions liberalization often aims at, may end up as third- or fourth-best solutions in reality.

Secondly, as the market develops, authorities are often slow to change regulation in an optimal manner. U.S. experiences tell us that the costs of policy making being slower than market dynamics may be significant. Thirdly, strong economic interests in firms to be regulated, lead these to lobby in order to prevent more competition and/or regulation. Fourthly, as European gas trade is international, also within a Maastricht-version of the European Union, the economic reasoning behind a possible opportunistic behaviour by one gas firm trading with firms in other countries may be supported by nation states which have a desire to maintain rent to the country and political influence following the firm's strong position in a market for an essential good like natural gas. Thus, liberalization of the Eureopan gas markets, may differ significantly between countries.

An important difference between the European gas market and many other markets being liberalized, is that natural gas is a non-renewable resource. With a limited supply, and prices (over time) to a large extent fixed by prices of alternative energies, there is an economic rent to be earned in the market, even after it is liberalized. The total rent is determined by the difference between market prices and the sum of cost of production, transportation, storage, distribution, gas use etc.. How this rent is distributed throughout the gas chain depends mainly on cost structures in firms, degree of competition (market power) in market segments and taxation policies. Rent may be redistributed between producers, pipelines and customers, respectively, as a result from the liberalization process. It may end up as governmental tax revenues and for shorter or longer periods as lower consumer prices, as well. The existence of, and fight over this rent among commercial and political actors, contributes to politicizing the European gas market more than most other markets. Partly for this reason, market liberalization should be viewed as a time-consuming process, where liberalization experiments will be in transition for a long time, rather than as a step from one static equilibrium to another.

Gas policies of the EU

The developement towards liberalization and regulatory reform taking place in Europe is not an isolated phenomenon. Over the past 15 years, a number of sectors in OECD economies have been liberalized. The U.S. and Canada were the first to liberalize their markets in the mid 1980s. Later, gas markets in the U.K., and then Australia and New Zealand, followed. In Continental Europe, steps have been taken to liberalize national gas markets in countries like the Netherlands, Italy and Spain.

The strong market concentrations and huge profits taken in the natural gas industry, particularly among transmission and distribution companies, could not be dealt with in Western Europe prior to the 1990s. Within the framework of the European Union's Single Market, intra-European trade may be discussed more easily, partly on multilateral and partly on a tentative supranational level.

The EU has, so far, proposed 3 directives aiming at a) a more transparent market, b) allowing transit of gas between high-pressure grids and c) introducing Third Party Access (TPA) to pipeline and unbundle their role as both merchants and transporters. Among these, TPA was not introduced after being proposed in 1992, due to heavy resistance from the industry and the European Parliament. It is, however, put on the agenda again in 1996/97, following the finalization of a similar directive for electricity decided upon in December 1996. With the proposal for a directive restructuring the community framework for the taxation of energy products in 1997, harmonization of energy taxation will probably be a reality, as well. This proposal suggests relatively sharp increases in minimum taxation on all energies, but relatively the most on natural gas (and coal).

Furthermore, in Norway, the EU attempts to increase competition among producing/exporting firms through the EFTA Surveillance Authority (ESA), which considers whether the GFU (The Norwegian gas sales monopoly) breaks competition rules within the European Economic Area (EEA). In court, an American oil company is accusing European gas firms for anti-competitive practices.

The electricity directive proposed is by many viewed as the opener for the TPA gas directive, as the gas and electricity markets have many similarities. It states that Member states may choose between two procedures to reach "objective, transparent and non-discriminating" criteria for the access to the electricity system (articles 17 and 18). One option is negotiated access based on voluntary commercial agreements. A country may also opt for a regulated system based on published tariffs. The other option is a single buyer procedure. A single buyer is a firm responsible for the unified management of the transmission system and/or for the purchasing and selling of electricity. According to the directive, the single buyer must publish its tariffs for the use of transportation systems and let eligible customers and producers use the system in contracts with each other. Either two options, give the transmission and distribution system right to refuse access to the system where it lacks the necessary capacity. The directive states that member states shall designate an authority, public or private, to be responsible for the organization, monitoring and control of the tendering procedures. The system shall be established gradually, in order to enable the industry to adjust to the common rules.

The EU initiatives aim at a more efficient gas market that should lower costs at all stages of the gas chain, improve security of gas supplies, reduce dependency on imported oil from the Middle East, and take the full benefit of natural gas' environmental advantages. In the area of taxation, it aims at moving taxes from labour as production factor towards energy (including natural gas). For exporters, the changing market and fiscal environment, may require a change in company strategy and become a challange for their international energy policies.

Pricing of European gas

Contractual price formulas in the continental European market are mostly designed to make prices react to changes in other energy prices with a time-lag, reflecting the value of gas for end-users. This value, or consumers' opportunity cost, represents a weighed average of their willingness to pay. Each end-user faces different alternative energies, either it is hydro or nuclear produced electricity, oil or coal (paricularly coal-fired electricity generation). This principle is valid for the pricing of gas both between producers and pipelines and between pipelines and customers at the city-gate. The price of gas agreed upon in these transactions is influenced by:

A change in the price on the alternatives to gas leads, rather automatically to a change in the sales price of gas to producers and to transmission networks, respectively. To a large extent, these prices are "net-backed" from the markets of alternative energies. Historically, the gross margins to LDCs and transmission companies (the difference between the prices they sell and they buy gas for) have largely been determined in a way that they do not vary with end-user prices. The margins to transmission companies are set by the negotiations with producers and customers, respectively. The pipelines attempt top "lock in" their initial profit margins and protect themselves from any fuel price movements. LDC margins are largely determined by the negotiations with transmission companies and the relationship between these prices and prices for gas in the market.

While a typical contract for exporters has a length of some 20 years, a typical contract for pipelines selling to their customers has a length of 1-5 year. In order to increase the market share for natural gas, in many contracts (such as for Troll) the initial relationship between the end-user price of gas and the price of the alternative energies is set to less than 1:1; that is, end-user prices of gas is set lower than the price of the alternatives. When pipelines write new contracts with customers, the price they agree upon is adjusted, in spite of the fact that they have signed more long-term contracts with exporters. That pipelines sell gas more short term than they buy, may give them a profit or loss compared to the initial situation. However, the pipelines are bound to take-or-pay (TOP) clauses with producers, determining that pipelines must pay for (a certain share) of the gas they have contracted, even if they are not able to sell the gas. Equivalently, the LDCs may regulate their prices to end-users according to what is possible to get from the market, in spite of the fact that they (too) are bound to more long-term contracts with transmission companies than they sell on.

Thus, the (net) price to the transporters depend both on the initial relationship between the gas price and the alternatives, and how the market (for each of them) develop within the contracted period. If gas can be sold at higher prices than expected in the contract period, transmission and/or distribution companies may benefit from that. The initial relationship between producer/pipeline and pipeline/customer prices, respectively, and the price of the alternative energies determines the base for the gross margins to pipelines and will be influenced by parties' cost of operation (fixed and variable), negotiation skill and market power.

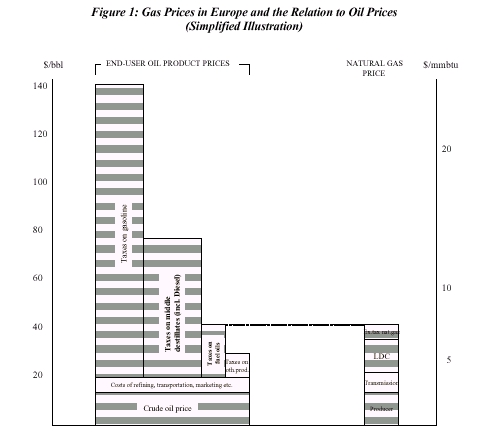

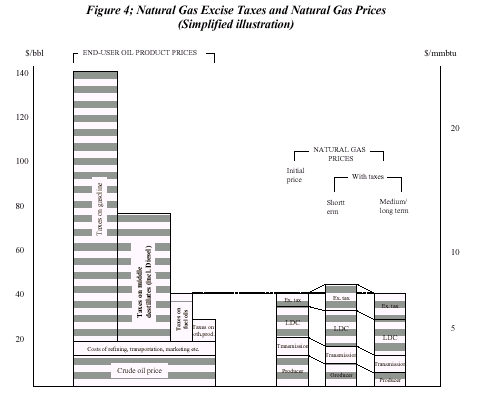

To illustrate the relationship between gas prices and the price of alternative energies we have, in figure 1, simplified the pricing mechanism to only reflect contracts where gas competes with fuel oils. We also disregard the more "short term" gains and losses transmission and distribution companies can make through changes in sales prices of gas within a contract period.

The left set of bars show end-user prices on oil products. The basis for these prices is the price of crude oil and costs to refining, marketing, transportation etc. In the figure, the crude oil price and the costs are illustrated as if they are equal across product types, even if this is not accurate. Our point, however, is that the main difference between the prices on different product types results from different oil product taxation. For a representative barrel of oil, our calculations have shown an average tax of 47 USD/bbl in OECD-Europe and an end-user price of some 70 USD/bbl in 1994 (see later sub-chapter). Gasoline has the highest taxation and would yield a per barrel price of some 140 USD in Europe, while taxes (and end-user prices) are falling on heavier products.

Usually, prices on crude oil are set in USD/bbl (a price per volume unit of crude oil), while prices on gas usually are set in USD/mmbtu (a price per unit of energy content of the gas). The ordinates to the left and right, respectively, illustrate the relationship between the two prices. The gas price bar to the right in figure 1, shows that gas prices to end-users are determined by the price of its alternatives, here fuel oils. The price of the alternatives to gas determines the size of the "cake" to be distributed between consuming countries governments (excise taxes on natural gas), distribution and transmission networks and producers (and, thus, the frame for producing countries' treasuries take from producers). As long as the margins to LDCs and pipelines are not reacting to changes in market prices, the price of gas to the exporter can be changed in the following ways (so far keeping taxes on gas itself constant):

From these mechanisms, it is often said that the producer takes the "price risk" and the pipelines take the "volume risk" in today's market. However, as long as price and volume are interconnected in a market, it is the producer that over time takes most of the risk connected with gas sales today. Nevertheless, it is thinkable that transmission companies face so many difficulties in selling gas to their customers, that they have to lower prices and/or volumes sold to an extent that the TOP-clauses become effective. In that situation, the companies involved may face a loss.

1) A higher crude oil price raises fuel oil prices and, thus, end-user prices on gas.2) Higher taxes on fuel oils also increase end-user prices on gas.

3) Higher taxes on all other oil products will, if they lower crude oil prices, lead to lower fuel oil prices, and, thus, lower end-user prices on gas.

4) If taxes on all oil products simultaneously are raised, it is not clear whether the taxes are under- or overcompensated of a possible lower crude price resulting. It is the composition of oil product taxation that determines whether or not gas prices benefit from increased taxation.

5) In case end-user prices fall, for one reason or the other, it is more or less fully reflected in a similar decline in producer prices.

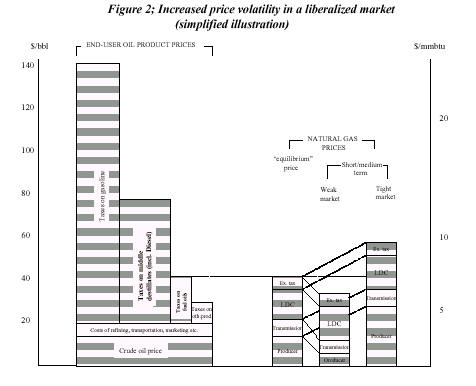

A more liberal market gives more volatile prices

In general, liberalization of the European gas market will increase the number of actors operating and transactions made in the market, as well as the speed of reactions in one segment to changes in another. For example, when producers and customers make direct contracts and pipelines are not acting as balancing intermediators anymore, market conditions may affect producers' prices more quickly. The number of actors increases and the volumes of each contract (at least for producers) decrease. Brokers and marketers may establish themselves to clear (parts of) the market, in addition to the direct contact between parties.

Prices (for exporters) become more volatile as they react to market

changes not only in the long term, but through gas-to-gas competition also

in the short and medium term (up to as much as 5-10 years). In a surplus

situation, a "gas bubble" would lower prices in short-term contracts. When

demand exceeds supply, spot and other short-term prices will be pushed

up. When a short-term market for natural gas is developed, it may work

as a barometer for the (underlying) trend in long-term prices. Depending

on how the balance between supply and demand develops, prices may actually

end up both below and above the prices within the existing system, as illustrated

in figure 2.

A tight gas market will produce more long-term, and a weak market more short-term contracts (including possible spot sales). With a higher number of actors and increased volatility, "long-term" in a new market structure will be shorter than in the existing system. More short-term transactions indicate greater variations in short- and medium-term prices depending on market tightness. How strong and quick responses will be, depends, besides on market conditions, on degree and shape of liberalization and firms' remaining market power. The increased number of short-term contracts will partly replace existing long-term contracts, but partly also satisfy customers not able to buy gas under today's system (with greater rigidity). Thus, demand may grow under liberalization.

Independent pricing of gas?

The question has been raised whether gas could be priced independently of its alternatives. Over time, that is not possible for any commodity. For example, in the U.S. gas prices have been lower than its alternatives for many years. However, these low prices were probably a result of the gas "bubble" existing after the mid 1980s, representing an over-supply in the market. As consumption gradually reabsorbed available production capacity, prices have been rising in the 1990s. Also in the U.S., the market value principle for end user prices of gas seems to be valid, even though differences may occur over the short- and medium-term.

However, if supply continuously overshoots demand, prices may remain lower than the price of the alternatives for longer time. This may, for example, happen if demand grows and the marginal producer makes economic rent even at low prices, and, therefore, continues to invest in new capacity. Similarly, if energy markets in general become tight and demand for gas overshoots supply, prices may over some time be higher than the price of the alternatives. The specific feature of natural gas markets is that such periods may last over number of years. In the European market, if supply prognoses are correct, a "gas bubble" may exist, which within a more liberal market structure more easily will lead to lower prices in the intermediate term.

Who wins - who looses?

If pipelines become regulated, or competition between them intensifies, gas from different sources meets in "gas-to-gas competition" at the customers level (at the city gate where LDCs, power plants and large industrial users buy their gas), rather than on importing countries' borders (where merchant pipelines buy their gas). If producers maintain today's market position (as oligopolists), and transaction costs are not too high, they should meet a weaker and more diversified group of buyers at the customers level than at today's monopsonistic import level. Customers should also be better off by meeting a somewhat more diversified group of exporters than the monopolist they face in the form of a merchant pipeline.

In this case, customers' purchasing price should drop at the same time as producers' price increases. This implies that customers and producers share the rent made available from increased competition between pipelines. For both producers and customers it will be important to maintain a purchasing position as concentrated as possible. The more market power each of them can get, the better off they may be in negotiations. If, on the other hand, exporting countries' selling monopolies are abolished or weakened, and today's purchasing pipeline consortium maintained, each company within a single producing/exporting country should sell gas directly to the purchasing pipeline consortium. This would improve the relative position of the merchant pipelines and should lower producer prices to the benefit of the pipeline.

Corrected for transaction costs, producers would benefit from selling gas directly to customers when end user markets are tight. Similarly, customers could benefit from buying gas directly from producers in a weak market. Thus, the process moving from one set/type of contracts to another as the market becomes more liberal, may take the form of various parties (including exporters/producers) claiming the termination or renegotiation of existing contracts (perhaps on a force majeure basis).

Thus, the changing market environment require adjustments of producers and customers company strategies. As contracts become more short term, diversified and volatile, an apparatus for closer contacts between them must be established. Spot markets, as well as hedging tools, such as futures and forward markets for natural gas, may develop. The ability to gradually develop such competence, in line with the liberalisation processes, will be an important factor for rent distribution between exporters and customers.

Theoretically, if no regulation of single firms takes place, but unbundling (throughout the gas chain) and price transparency are introduced and horizontal collaboration is made illegal both between producing companies and pipelines, this should have the potential of increasing the relative market power to pipelines. This is due to the assumption that pipelines have greater elements of natural monopoly (economies of scale and/or scope) than do producing companies. Thus, the most significant threat to pipelines' profit may be an actual regulation of the terms for operation, rather than increased competition, unless competition takes place only in the transmission segment. Eventually, if regulation of transporters behavior is introduced, LDCs and pipelines may become more concerned about how regulation is made and may try to "trap" the regulator to serve their interests, rather than just oppose him.

To the extent that the European Community represent the "collective" interests of member countries, the EU could have incitement to make decisions conflicting both with single firms, regions and countries interest in order to maximize "Community wealth". In particular, the EU (as a group) would have interest in intensified competition and in regulating tariffs and terms for operations in situations where costs are carried by non-EU exporters.

For example, if nothing else happens than that competition increases between gas sellers / producers / exporters, pipelines' market position will be strengthened and profit transferred from producers to transporters (in new contracts). For example, this may be the effect if the ESA control committee finds the Norwegian sales monopoly (GFU) illegal according to EU/EEA competition rules and no other "liberalization" steps are taken further down the gas chain.

If the TPA directive is introduced, similar to the electricity directive, there will be some sort of a negotiated access to the grids based on commercial agreements. At the time two parties do not agree about terms, the deal must be sent to EU authorities (e.g. the Court of Justice). Thus, a TPA directive may be the forerunner for an access arrangement to the pipelines based on some sort of regulated tariffs. Whether or not this happens, the role of the pipelines will be weakened and the customers will benefit. Producers may benefit or loose, depending on their ability to write new contracts directly with the customers, terms for pipeline transportation, market developments and taxation policies.

The Take-or-Pay (TOP) Provisions

Today's long-term contracts are now "securing" exporters a market for their gas. From producing companies view, one argument against liberalization has been that it will erode the security of volume offset. However, the stability provided by merchant pipelines in today's system is based on a stable demand on natural gas. Obviously, this gas can be sold directly to customers (or via a brokerage or marketing firm) as well as through a pipeline intermediate. Furthermore, nobody knows what will happen with pipelines' take-or-pay obligations if they are not able to sell the contracted gas under today's system, for example in a situation with strong decline in demand. Price and volume in a market are interconnected. Usually, a volume can be sold if the price is sufficiently low. Thus, the risk that customers should not be able to purchase gas, or that exporters should not find buyers, as result of a changed market structure, should not be overestimated.

However, a more liberal market may provoke a revision of the existing contracts. Competition among pipelines or regulation of terms for operation lower their profit margins, at the same time as the volumes and the prices at which they can sell gas to customers become lower. This may indicate that there is only a question of time before the existing merchant pipelines will claim renegotiation of the terms under which "old" contracts are signed with exporters. If the contract structure should be maintained, with continued sales of gas from exporters to the pipeline, with the only change that price and contractual should reflect the new and more competitive market for pipeline selling gas at the customers level, exporters run the risk that the entire downward pressure in prices to customers will be paid by them, without them getting the benefit from lower margins under which the pipeline operate.

However, from another point of view, unless the old merchant pipeline lower their margins to the level of the new one, exporters may claim force majeure negotiations, because contracts no longer reflect market conditions. Exporters could be better paid by selling gas directly to customers. At this stage, the pipeline may benefit from changing their strategies from resistance against a more competitive environment, to influencing how the liberalization process takes (to trap "the regulators decisions). This would cost the old pipeline market shares and profits, but less than if no collaboration takes place.

Thus, either way, the existing TOP clauses will come under pressure as the market becomes more liberal. As producer prices in "old" contracts are linked to end-user prices of gas (not to pipelines sales prices to their customers), these contracts may be maintained if pipelines accept lower margins. The question is, whether or not they can argue that the market environment is changed so much that force majeure provisions may be enforced.

If pipelines transporting and merchant functions are unbundled and their margins are competed or regulated down, they may be unable to fulfill their obligations towards producers in existing TOP clauses. These experiences were made in the U.S. in the mid 1980s after the introduction of Open Access under Order 436 simultaneously with the oversupply of gas and of pipeline capacity in the market. Pipelines' stabilizing brokerage function must be taken over by producers and customers through a greater and more diverse contract portfolio. Many of the existing contracts must be replaced with new contracts between producers and customers.

Are U.S. Experiences Relevant for Europe?

The most striking difference between the European and the U.S. gas market is that in Europe, there is strong power concentration (few firms operating) at most levels and segments of the market, while in the U.S., it is controlled by thousands of producers and numerous distributors. While the typical pipeline in Europe faces oligopoly and oligopsony at it's entrance and exit, the typical U.S. pipeline faces something closer to competition at both ends.

In Europe today, international trade of gas must be negotiated bilaterally, as inter-state trade in the U.S. before the Natural Gas Act (NGA) in 1938. The potential role of the EU Commission in intervening in (parts of) the market may parallel the U.S. federal government's role in regulating the inter-state trade at that time. However, even more than 50 years after the first regulations passed Congress in 1938, the U.S. gas market still suffered from undesired inequities. The wishes of the Congress were not always enough to make the market conform to it's desires. Repeated regulations and deregulations have often lead to undesired results with dramatic stop-and-go policies following.

These experiences reflect the difficulty in finding optimal schedules for the liberalization of any gas market. Regulations should be made with a consciousness of the market framework and mechanisms and how these may evolve. Placing a lot of this judgment on policymakers and lawyers, may create inefficiencies in Europe, as it has in the U.S.. If it is possible to find self-regulatory mechanisms, the damages on the economies made by misjudgments and inefficiencies created may be reduced. It is also worth observing that the choice of doing nothing probably has been considered the worst possible solution in the U.S. Few suggested that the situation that existed before the NGA was implemented in 1938 was better than the more or less regulated situations after.

Due to the need for and complexity of regulations of natural monopolies there may be a parallel need in Europe as in the U.S. to oversight a "completely liberalized market" with quite a substantial regulatory authority. The regulatory techniques in the U.S., as exercised by the Federal Energy Regulatory Commission (FERC), may be of some help in designing regulation in Europe, even though they are not necessarily directly applicable. So far, a supranational agency to deal with gas market regulations, like the FERC, is absent in Europe. Most agencies will remain national, while the EU will provide a looser framework for national legislation and regulation, than the federal FERC.

The EU is not a federation, and is only moving (in the long term?) towards a confederation. Trade is international, and will continue to be so. Not least, however, this is due to the fact that much gas will be imported from outside EU jurisdiction in the foreseeable future. In the U.S., only a minor part of consumption is imported. This lack of a juridical body to deal with the entire market, limits the possibilities of a full liberalizing of the European market. The fact that trade crosses nation states outside and inside the Union, with all their differences, reinforces the problems of dealing with diverging economic interests. It indicates that, within a possible EU framework (with the TPA directive as a starter), many national solutions will be found, reinforcing the need for a gradual liberalization, rather than one that aims at reaching the goals in only a few big steps.

Another lesson to be learned from the U.S., is that a more liberal market leads to greater and more frequent price variations, even though competing energy markets put limits on these variations in end-user markets on the upper side and costs of production on the down side. However, the drop in U.S. prices in the late 1980s was not necessarily caused primarily by liberalization, but perhaps the "Open Access" system introduced made reactions stronger and faster. Lower oil prices and oversupply of gas (the "gas bubble") forced prices down. In the 1990s, U.S. gas prices have been rising due to a better balance between supply and demand.

Energy taxes

As already discussed, taxation of alternative energies to gas, in general, and oil products, in particular, influences gas prices rather directly. The question now is, what happens if gas taxes themselves are raised? Due to the environmental advantages of gas, compared to oil, and in particular, to coal, this issue has partly been disregarded by many analysts. For environmental reasons gas should be taxed less than other fossil energies.

However, the EU directive for the taxation of energy products was proposed in spring 1997, right after the renewed emphasis on the TPA directive, and suggests substantial increase in gas taxation. The proposal gives a framework for "enabling a revenue neutral restructuring of tax systems to sustain employment and the environment". It aims at "modernizing the Community system for the taxation of mineral oils and extends its scope to all energy products". The measure is a harmonization of energy taxation, and the proposal suggests the introduction of minimum charges on the use of all energies. Following "the deadlock of negotiations on the CO2/energy tax", it suggests reducing statutory charges on labour replacing it with higher energy taxes. The directive proposal moves the emphasis from the environmental benefits of natural gas towards the nations need for revenues and competitiveness. It offers Member States to a greater use of energy taxation for environmental purposes, but in particular and in favor of labor as a factor of production in a "revenue neutral" manner. It "states" that consumers will be very little hurt by the sharp tax increases suggested. The minimum charges should be introduced in 1998, and raised step-by-step until 2002, when a new escalation plan may be put on the agenda. The minimum rate for natural gas shall be increased as much as 350 per cent in the period 1998-2002.

To illustrate the important role energy taxation now is playing for energy markets, we shall take a short look at what has happened in this area in the oil market over the last decade. The directive for increased CO2 taxes, mentioned in the EU tax proposal of 1997, was proposed by the EU in 1990. It suggested a 10 USD/bbl increase in the taxation of oil by the year 2000. The directive was not implemented. and more or less it was not necessary; Already in 1993, the tax increase suggested was implemented in the major European industrialized countries. In some cases, it was vastly exceeded.

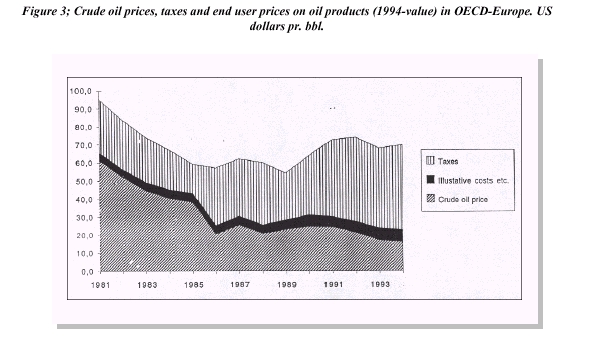

EU countries have been the forerunners in increasing oil product taxes.

To demonstrate their willingness to tax, even without directives saying

they shall do so, the different development in oil prices to consumers

and producers, respectively, is shown in figure 3. After the drop in crude

oil prices in 1985/86, today's real value of a barrel of crude oil is about

one fourth of the value at the beginning of the 1980s. Since the Gulf War

in 1991, real crude prices have continued to drop, to some 2/3 of the 1990

value (with the exception of autumn 1996). Prices to consumers have, on

the other hand, been much more stable. In real terms, EU consumers now

pay about the same as they did in 1986.

In real 1994-terms, the price of crude oil decreased from 61 to 16 USD/bbl

in the period 1985-1995. In OECD Europe, the decline in prices of 46 USD/bbl

has partly been compensated for by an increase in taxes of some 20 USD/bbl.

On average, in Europe, the amount of taxes on a barrel of oil was some

47 USD/bbl in 1994, against 20-30 USD/bbl in the early 1980s. Thus, in

spite of the dramatic drop in crude prices, the average price to consumers

decreased (only) from 95 to 70 USD/bbl, as shown in figure 3. As per centage

of end-user prices, the typical tax in 1996 was 70-80 % on gasoline, 50-60

% on diesel and 30-70 % on light fuel oils. Probably, these taxes have

contributed in depressing crude oil prices in the period. There is now

an assymetry in the response of product demand to changes in the crude

oil price. While crude prices are dropping, product prices are stable or

rising. Therefore, analyses of demand for oil must modified with respect

to product taxation.

Effects of Gas Taxation

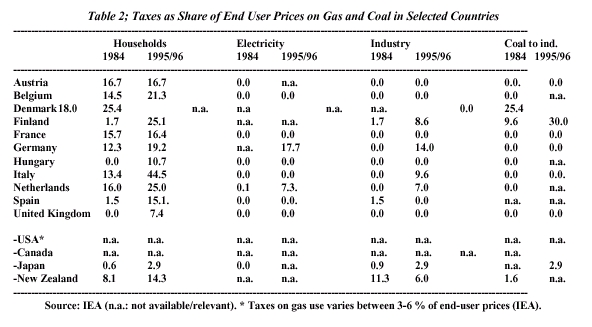

So far, gas prices have benefited from the sharp increase in oil product taxation., while taxation of gas has been more moderate. As percentage share of end user prices to households, they have increased from some 15 % in 1984 to slighly more than 20 % in 1994 in many countries (table 2). Taxation of gas to power plants and the industry is lower, in many countries zero. Even though gas taxes are low compared to oil product taxation, taxes on polluting coal is even less, in fact coal is subsidized in many countries. This tax-structure reinforces the impression that energy taxation in consuming countries has primarily not been set with reference to the environment, but first of all from fiscal needs, often as replacement for lower income taxes.

A tax creates (or increases) a difference between the price producers receive and the price consumers pay. In general, such a tax is partly borne by producers (through lower prices) and partly paid by consumers (through higher prices). It will always be the one side that is least elastic that pays most of the tax. For example, if demand is more elastic than supply, more than half of the tax will be paid by producers. If supply is totally inelastic with respect to prices, producers pay the entire tax (and vice versa) et.c.

If gas taxes are raised, a first effect could be that the increase is partly producer and partly consumer paid, as shown in the middle gas bar in figure 4. However, as consumer prices over time cannot be higher than the price of its alternatives a tax rise must, eventually, push prices further up in the gas chain down,. In the short term it is possible that the tax is partly paid by end-users, depending on how (in)elastic demand for gas is, and whether end-user prices matches its alternatives initially. If gas prices initially is lower than the price of its alternatives (in order to increase gas' share of overall energy demand), consumers may pay the tax more permanently at the cost of a lower growth in gas demand. If the transporters (pipelines and LDCs) take a higher price for gas than what the initial relationship between gas prices and its alternatives presupposes, the transporters may also pay the tax in the short term. If, however, demand growth should be maintained, or the market is matured in a way that end-user prices on gas equal prices on its alternatives, the tax must, eventually, be paid by producers or the transporters through negotiations.

How these negotiations end up depend on parties' cost, negotiation strength/market

power, jura etc. As already mentioned, historically, transporters margins

seem rather independent of end-user prices in the negotiations. As long

as transporters can argue that the level of their (rather high) existing

margins are necessary to cover costs, an increase in taxes will not be

borne by them. Thus, in the case with fixed margins to LDCs and pipelines,

a gas tax must, eventually, be borne by producers. This is shown in the

third gas bar to the right in figure 4.

The less dependent margins to pipelines and LDCs are on end-user prices, the more of the tax, if not all, must, eventually, be borne by producers/exporters. Probably, the result is that, over time, a new gas burden is shared throughout the industry and contributing in bringing end-user prices equal to its alternatives (1:1) if they are not there today. In the case of liberalization, there may be a redistribution of rent within the gas chain. In the case of taxation, money is transferred from the industry and to consuming countries governments treasuries. Thus, the natural gas industry may more easily oppose the taxation directive than the TPA (and following gas) directive(s), as it puts a pressure on all margins thoughout the gas chain. In case of of liberalization, some may loose and some may win.

Limits to Gas Taxation

One limit to gas taxation, at a given status of the market, will be determined by the cost of getting new gas to the market (long term marginal cost of gas production). The higher the ambition of increasing gas consumption, the lower the taxes must be. But producer prices need not be higher than what is "necessary" to make producers invest in new capacity. As long as some rent, with "reasonable certainty", is left to a producer making calculations for new field developments, he will invest if he consider himself as a price taker. At the end, the only fields making economic rent may, eventually, be those of low cost. Furthermore, the more cost effectively producers can operate, the higher taxes can be, as well. Thus, an owner of an exhaustible resource will, over time, not necessarily earn economic rent, even if consumer prices are rising.

At a given margin to transporters, the long-run marginal cost (LRMC) of bringing new gas to the market will set a limit to how low producer prices can be, and, thus, put a ceiling on gas taxes. If the share of natural gas shall continue to grow, exporters' prices should be higher than if consumption should remain stable. This may particularly be the case if new gas should come from Iran, Kazakhstan, northern Norway and Siberia (at least if Russian economy develops as a market economy).

Between sectors, there may be different limits to taxation. Industries that use gas are in regional or European competition in using gas as an input factor. In the product markets, however, they are to a larger extent in global competition, in the same way as industry using oil as an input factor. Private households do not compete in global markets, but choose their energy (mix) according to relative prices (including taxes), technology, cost of switching between energies etc. This uneven competitive position across gas consuming sectors may imply that taxation on gas use in households/business will remain higher than on use in industry and power plants. Tax rates will depend on technology in the use of gas, as well.

With oversupply in a more liberal market, gas-to-gas competition may force prices to customers and consumers down. If gross margins to LDCs and pipelines, respectively, are fixed, producer prices will be pushed down. In this situation, taxes must be lower than in a situation where gas prices equal the substitute price, in order to give producers a price that covers cost. However, in the "long run", end users price of gas must equal the price of its alternatives. As long as gas prices are lower than prices on the alternatives, more users will switch to gas. Since we are facing an exhaustible, non-renewable resource, at some stage supply increases must take an end, and prices to users again equal prices of its alternatives. On the other hand, as long as "long-run" in the gas industry may be 5-10 years and more (as in the U.S.), a situation where supply continuously overshoots demand may put a limit to taxation for a rather long period.

If, however, energy taxes to a larger extent than today are set to reflect each carriers environmental benefits and costs, taxes on gas should be low, and taxes on coal increased (and subsidies removed). Among fossil fuels, natural gas is the environment's best friend. The removal of coal subsidies should increase demand for gas. The price of gas should, however, remain the same as its alternatives. A (theoretical) removal of all gas taxes should, therefore, not increase gas consumption through lower prices to consumers. Low gas taxes would benefit producers (and possibly transporters) through higher prices and consuming countries through continued increases in supplies.

Within such limitations (and temptations), gas taxes may become revenue generators for consuming countries governments in the same way as oil product taxes are. At least, if (most of the) gas taxes eventually are paid by a transfer of economic rent from producing / exporting countries, there seem to be few reasons why consuming countries should not optimize the gas tax portfolio, with respect to the limitations set up.

An increase in gas excise taxes may become particularly attractive for consuming countries' governments when rent is made available in the gas chain, whatever the cause. This is what has happened in the oil market over the last decade. When crude oil prices dropped in 1986 and 1991, consumers could have derived the benefit from the loss of rent among producers. However, consuming countries raised oil product taxation, which stabilized end-user prices on oil and suppressed a potential later price rise on crude oil. As downward trends in crude oil prices can be used to increase oil product taxation, while an upward trend can be used to increase gas taxes, energy taxation as such may become a major political challenge for both oil and gas producers in their relations to importing countries.

Taxation and Market Liberalization

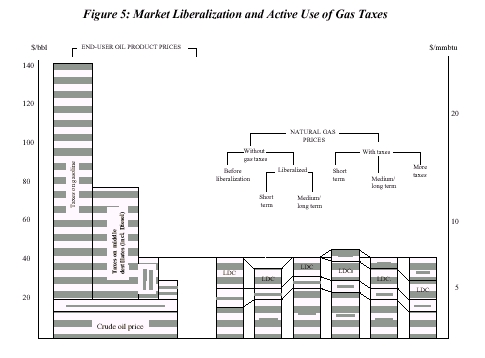

With no tax changes, regulations of LDCs could benefit transmission lines and/or exporters (depending on the remaining market structure). Regulation of pipelines could benefit exporters and/or customers. In these cases, local and national authorities may be better off by leaving the rent in the local or national company, rather than sending it (in most cases) out of the region or abroad. Then, it may seem better to leave the market "unregulated". If, however, these authorities can collect the rent made available through taxation, the desire to regulate down margins in transmission and/or distribution could be reinforced.

In the simplified illustration in figure 5, the second gas bar shows successful regulation of transporting companies, to the benefit partly of consumers and partly of producers. The third gas bar shows that end user prices eventually must match their alternatives, and be raised to this level after some adjustment time. With fixed margins to LDCs and pipeline companies, this must benefit producers.

An increase of taxes in this situation may be partly paid by consumers through higher prices and partly by producers through lower prices, as shown in the fourth gas bar. Eventually, as long as end user prices must match the price of their alternatives, this tax must all be paid by producers. In fact, taxes may be increased to the level that producers make only normal profit, as illustrated at the gas bar furthest to the left.

One important question is whether transporters will be able to argue that their often huge profit margins are necessary in order to maintain operation. As margins are being pressured, it seems likely that also pipelines and LDCs must pay some of the tax. Aslo consumers can pay some of the tax, especially as long as some gas is priced under its alternatives in order to penetrate the market. In these cases, the tax may lead to slower growth in gas usage (at the extreme; zero growth or declining consumption).

Less new gas to the market?

From a consuming countrys point of view, a downstream liberalisation of the market only (from the gas enters the EU area), there is a risk whether there are enough sellers to create a real market with competition or whether the oligopolistic exporting countries will be able to enforce an anti-competitive situation. Our analysis, concludes that this concern may have some validity, but only under certain assumptions. For producers, it is a genuine risk connected to the increased uncertainty and price volatility a more liberal market creates, in general, and of the possibility of increased gas taxation, in particular.

A (theoretically) completely liberalised market prerequisites competition between exporting firms., which is not the case today. Joint operation of gas fields and transportation within exporting countries is important in order to exploit the benefits of economies of scope. One scope benefit is in horizontal integration across producing fields when determining optimal extraction paths taking into consideration the fact that natural gas is an exhaustible resource. Another scope benefit is that of vertical integration among exporters and (importing countries') transmission lines in orchestrating production and transportation to the market, as represented by the long term TOP contracts. A third scope benefit is of resource management kind, and the orchestrating of many smaller contracts in one merchant and production management. Coordinated gas sales and production can be maintained and developed in several ways, including competition between exporters of single fields and regulation of exporting countries pipelines. The point is that, from a producing country's point of view, it is important that some institution have the overall view on the benefits of economies of scope, distribution of rent throughout the gas chain and other commercial aspects of exporters' competitiveness.

As prices in each contract may vary more, and contract lengths may become shorter, the increased volatility and diversity require a greater dynamism and apparatus both among exporters and customers in order to operate competitively in a more liberal market. "Price risk" in a new system will be taken by producers/exporters, as in today's system, and pipelines and LDCs will continue to operate under low risk but under lower profit margins and costs. Prices to exporters may become higher or lower than under today's system depending on the use of gas taxes, but uncertainty will be greater.

Worst case scenario for exporters occur when fields and pipelines are "fully" developed. At this stage, most producers' costs are sunk, and producers have no alternative but to continue supplying gas through existing facilities and grids even though prices are well below what was expected. In the extreme, if no new capacity is available, taxes could be raised to the point where producers' prices just cover a little more than variable costs. With all cost sunk, producers would benefit from continuing producing even if prices do not cover fixed costs.

This situation may lead to a new situation in the development of exporter's new mega fields and pipeline projects. Financing gas projects could, in general, become more dependent on the financial community's assessment of the long term risk in the market, rather than based on fixed pre-sales of gas. It could also lead to different ways of sharing risk, such as customers being engaged in upstream activities, exporters and customers engaged in new pipeline projects, and exporters in LDC and gas power plant developments. Under liberalization, investment decisions may (in principle) become more similar to those of mega oil projects, where the price risk exists, as well, and the volumes are sold spot or on terms of a few months. For the development of giant oil fields, exporters should be able to borrow money by financial institutions in the belief that the market for oil will yield revenues that make the oil company able to cover repayments.

For producers, it is important to get time to develop the expertise and network to make a large enough portfolio of contracts to defend (the huge) investments. Liberalisation will require more direct contacts with customers and greater activity in the markets to (partly) replace the broker role of transmission companies. Furthermore, access to storage facilities is crucial to be able to supply customers on a regular basis.

Secondly, increased price volatility due to liberalisation requires higher expected profit in the investments as compared to today's more stable prices. In a liberalised market, the financing of new huge gas field developments will probably look more like the situation when oil fields are developed. Today, ex ante, the huge contracts to a large extent guarantee for investment costs

Thirdly, and probably most problematic, is that purchasing countries through energy taxes have a political tool that, ex post, can derive (much of) their expected rent. Therefore, one element that should be included in future contracts is decisions over how a tax burden shall be shared within the industry. It is, however, difficult to limit future parliaments' ability to put new taxes on the use of gas. If the gas tax instrument is used to a larger extent than today, producers are not anymore facing market prices only, even in a liberalised market. With an active use of gas taxes, prices are heavily influenced by political decision making. If this situation cannot be solved, producers may not be able to take the price risk anymore, and, consequently, delay huge new investment projects.

Thus, a challenge for exporters on the political level is how to influence the way the market is liberalized, in general, and how energy taxation develop, in particular. As the three major exporters, Algerie, Russia and Norway, are rather different non-EU members, this may prove difficult. On the other hand, whether this will lead to more discussions between them in in cooperation about export strategies, is yet an open question.

Conclusions

The process towards a more liberal European gas market is partly driven by increased competition, due to market growth, investment in new transportation routes etc., and partly led by political decision making on national and/or EU levels. Jonathan Stern (1992) argues that the common rules from the EU only will provide a "loose frame of reference" for national governments. He also argues that the process will gradually evolve, more lead by market players than driven by regulators. In his view, liberalization (or TPA as Stern discusses) will develop on a country-by-country and case-by-case basis, which over time may lead to a more equitable and uniform regime, rather than initiated by a supranational EU body. Stern's arguments seem valid within the context of the discussion above.

However, local and national authorities could desire (if otherwise politically possible) to use their visible hands to regulate margins in transmission and/or distribution down sooner if they can collect the rent made available themselves, for example through taxation. The recent proposal on revisions of energy taxation may be a step in this direction. Taxes could be put on consumers as well as on transmission and distribution services. With no tax changes, regulations of LDCs would benefit transmission lines and/or exporters (depending on how the market is liberalized). Regulations of pipelines would benefit exporters and/or customers. In these situations, local and national authorities may be better off by leaving the rent in the local or national company, rather than sending it (in most cases) out of the region and/or abroad and leave the market unregulated if taxes could not be increased.

An increase in gas taxes is particularly tempting when the price of the alternatives to gas are increasing. In our illustration this could take place when either crude oil prices or taxes on oil products are increasing. For example, Italy increased gas taxes substantially at the end of the 1980s as a joint policy with the increase of oil product taxes. If consuming countries consider that "enough" rent is given to producers of gas, implying that producers continue to invest in new capacity at current prices, there should, from this point of view, be no reason to give away economic rent by not increasing taxes on consumption.

If gas taxes are increased simultaneously with the use of invisible and visible hands that reduce profit margins and improve cost effectiveness in transmission and distribution companies, the EU may more easily get support from national governments in proceeding with the liberalization process. An active use of gas taxes as a strategic instrument to derive rent, increases the probability of a politically led liberalization process both on local, national and EU levels.

The question is, however, whether such a policy will give enough gas to the market in the next century. Liberalization requires a change in company strategy among exporters. Exporters need more downstream acitivities in order to remain competitive, downstream investments and marketing included, as the market becomes more liberal. By doing this, exporters may not necessarily loose on liberalisation and supply growth may continue. However, if the tax instrument is used actively in the market, the political price risk run by exporters may become significant. This may delay huge new sunk and long term investments, the market being liberalised or not.

Any movement in crude oil prices can be used to increase taxes either

on oil products (when crude prices are dropping) or on gas (when crude

prices or oil product taxes are increasing). As it is producing countries'

governments that take most of the rent on the supply side, and consuming

countries' governments that take most of the rent on the demand side (both

through taxation), energy taxation should become a conflict of interests

first of all between producing and consuming countries governments.

LITERATURE

Austvik, Ole Gunnar, 1996a; Avgifter tar forskjellen; Olje- og gassprisene faller, mens forbruksprisene holder seg, HIL-paper no. 17 / 1996 Lillehammer College April/October. ISSN 0806-8348. Avgifter og petroleumspriser: Tar konsumentlandene olje- og gassinntektene?, Sosialøkonomen no 5. Mai 1996 ISSN 0038-1624

---, 1996b; "Liberalization of the European gas market; The Workings of Invisible and Visible Hands", Report from a research project under the Norwegian Research Council. 211 pages. HIL-paper no. 31 / 1996. (Working Paper Lillehammer College) November. ISSN 0806-8348.

Broadman, H., 1986; "Elements of Market Power in the Natural Gas Industry", The Energy Journal, Vol 7, no.1

European Union, 1988; The Internal Energy Market, Commission Working Document, May

---, 1990; Council Directive of 29 June 1990 concerning a community procedure to improve the transparency of gas and electricity prices charged to industrial end-users, CEL-Title 90/377/EEC

---, 1991; Council Directive of 31 May 1991 on the TRANSIT of natural gas through grids, CEL Title 91/296/EEC

---, 1992; Proposal for a Council directive concerning common rules for the internal market in natural gas (Third Party Access, TPA, directive), Com 91/548 Final SYN 385.

---, 1996; Directive 96/92/EC of the European Parliament and of the Council of 19 December 1996 concerning common rules for the internal market in electricity.

---, 1997a; Amended Proposal for a European Parliament and Council Directive Concerning Common Rules for the Internal Market in Natural Gas, 5793/97 Limite Ener10 Codec73. 04.02.1997

---, 1997b; Proposal for a Directive Restructuring the Community Framework for the Taxation of Energy Products, COM(97) 30 final 97/0111(CNS), 12.03.1997.

International Energy Agency (IEA), 1994; Natural Gas Transportation; Organisation and Regulation, Paris

Ministry of Oil and Energy (MOE), 1997; Memorandum on the Establishement and Functioning of the GFU, Oslo 20.01.1997

Noreng, Øystein, 1994; Liberalisering av det europeiske gassmarkedet, Report to Ministry of Industry and Energy (with contributions from Ole Gunnar Austvik), u.o.

Reinsch, A.E., Considine, J.I & MacKay, E.J., 1994; Taxing the Difference, Canadian Energy Research Institute Study no. 59 ISBN 0-920522-91-1

Stern, Jonathan, 1992; Third Party Access in European Gas Industry; Regulation-driven or Policy-led? Royal Institute of International Affairs, London ISBN 0 905031 371.