|

Political

Gas Pricing Premiums. OPEC Review no. 2 June 1987 pp 171-190 ISSN no. 0277-0180.

Download full-text as pdf-file. |

Keywords: x

Introduction

Many people have claimed that the danger of disruption of supplies

of natural gas from the Soviet Union to Western Europe must lead to

increased

Norwegian production to supplant Soviet export. This is an

argument

which has been put forward as particularly applicable in a situation

where

the "normal" tempo of development of Norwegian gas fields, and a

decrease

in Dutch production, would lead to a disturbingly large share of

imports

having to come from the Soviet Union. It is claimed, especially

from

the Norwegian side, that in order to increase our production faster

than

the so-called "normal" plan; Norwegian gas would have to be priced

higher

than Russian gas.

In order to see if any such preferential pricing has in fact been implemented, I shall in this paper show a comparison of prices on supplies of natural gas from various countries to West Germany, and discuss various opinions regarding the possibility of any type of preferential involving the participants in the market.

Companies and government authorities are extremely reticent about allowing gas prices to be revealed to the general public, and price both in previous and in future contracts are only referred to in more or less general terms in a number of specialist magazines. In official trade statistics, too, prices are kept secret in many countries by means of suppression of figures related to quantity or value, distribution by country or combinations of these. This secrecy hampers a discussion about the reality of a preferential gas pricing.

A great deal of data suppressed in statistics may however be decoded by comparing different information. As far as gas prices are concerned we have, by utilizing statistics published by the Statistisches Bundesamt under different nomenclatures, arrived at quantities, values and thus prices of the gas West Germany has registered as imported from each individual country. The advantage of using such a source is that each import figure is based on invoice values, converted to a price c.i.f. the German border. This makes prices comparable even if the contracts contain different processing values. They may however conceal considerable differences in individual contracts. The figures only provide average prices, gauged in proportion to the quantity supplied in accordance with each individual contract. Such a survey does, of course, not provide an answer to the question of whether preferential pricing is an integral part of future contracts.

In the first chapter of this paper there will be a discussion concerning how factors connected with economic and political dependency may be imagined as influencing consumption of the individual energy sources and their distribution in terms of country. Then there will be a presentation of various reasons why differences in prices can arise considering the manner in which gas contracts are normally formulated. In the second chapter the prices of supplies of natural gas to West Germany from the Soviet Union, the Netherlands and Norway respectively in the 1977 85 period will be compared. It is evident that the proportionally gauged average prices from the individual countries seem to tend toward being comparatively similar over a period of time. In other words, any preferences for individual exporters have so far not been reflected in prices. Various possible reasons for this will be discussed. In the third chapter possible developmental trends in the future will be discussed, among other things how preferences for certain countries may be imagined as having other effects than differences in price setting. The main features concerning calculations and methodic are described in a separate appendix.

Gas contracts and uncertainty in utilization of energy

All utilization of energy involves risks. Nuclear power involves the

possibility of accidents. Coal involves a pollution problem. Hydro

electric

power is probably the least risky source of energy, even though it

depends

on precipitation. All import of energy also involves to a greater

or lesser degree of risk of political and economic dependency in the

exporting

countries. In particular this is a problem that has been focused

strongly

on with regard to oil and gas. This leads to a situation where on the

one

hand countries wish to diversify consumption among several energy

sources,

and, to the extent that they are dependent upon import of individual

sources,

also among several supplier nations.

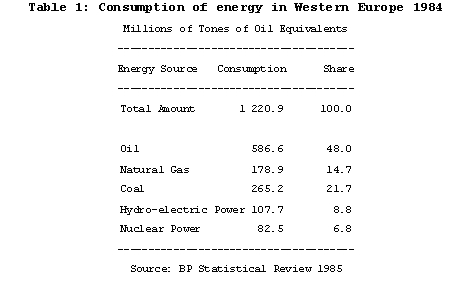

Western Europe's dependency on oil is considerable, a thing which in itself is an incentive to move in the direction of greater utilization of other energy sources. One way to substitute oil is using more natural gas. In the European gas market consumer countries have the possibility of dividing their purchases among the Netherlands, Norway, the Soviet Union and North Africa. Other areas gas may be supplied from are the Middle East and other African countries (such as Nigeria), but this does not seem realistic before some way into the next century.

In recent years Western Europe has experienced increasing

consumption

of natural gas. In 1984 consumption was approximately 214 billion cubic

meters (approximately 178 mtoe), which partly has been the result of a

deliberate policy of reducing consumption of crude oil. The main

consumer countries are France, Italy, Great Britain and the Federal

Republic

of Germany, with the Netherlands playing a double role as a major

producer

and consumer. The Soviet Union is the dominant producer in the

"region",

though most Soviet production is consumed domestically. Since

production,

then, takes place in areas other than those where a significant amount

of consumption takes place, significant trade flows arise, where

pricing

and the reliability of supplies are important both to exporters and

importers.

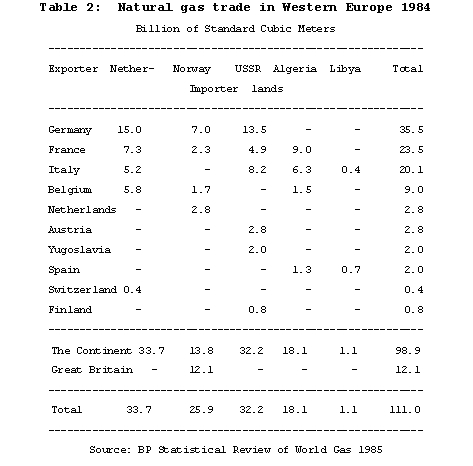

Approximately half of West European consumption is covered by imports. In continental Europe the Netherlands and the Soviet Union are now approximately equally large exporters. However, if one looks at the whole West European import picture (including Great Britain), Norway is just a bit smaller than each of the other two. The newly signed Troll contract will raise Norway's export figures till today's level of the Russian's and the Netherlands in Continental Europe.

The validity of the argument that a country should receive a special political preferential price for its gas exports depends among others upon to what extent other suppliers are regarded as being unreliable, what developments take place in other energy markets, what developments take place in western economy, to what degree economic activity leads to increased demand for energy, what capital equipment utilizing individual energy sources in individual countries is like, and not least: what price the market will "give" without intervention having taken place.

With so many variables influencing the validity of the argument, there may, at least theoretically, be situations where preferential pricing is realistic for one country, situations where no country will receive a preferential price and situations where preferential treatment may be based on aspects other than prices.

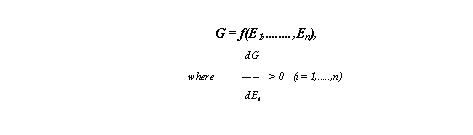

Prices in contracts for the sale of natural gas are positively correlated to prices of other energy sources contained in the contract. If the price of gas is G and the price of other energy sources Ei (i = 1,....n) the price of gas may be expressed generally by the following formula:

The main element of the philosophy behind formulation of contracts where prices are linked to other energy prices is based on the idea that gas prices should be more or less the same as the prices of the energy sources gas competes with. However, if one is to replace other energy sources with natural gas one must set gas prices somewhat lower than the prices of alternatives, so that transitional costs are also covered. The degree of this depends, among other things, on how fast one wishes to replace the capital equipment compared to its living age.

The price of alternative energy sources also varies with the sector it is delivered to. It is lowest for electricity supplies, somewhat higher for industry, and highest for general supplies to households and businesses. The price we will be referring to later is gauged in proportion to the quantities contained in the various areas of utilization. Thus relatively greater utilization of natural gas in households would push the average price up. In the same way a technical modification in one of the areas of utilization would increase the value of the gas to users. If the negotiated price is focused on the average price, re negotiation, then, should take place each time such technical improvement or changes in connection with market distribution take place, if one is to retain a price similar to that for alternative energy sources as a whole.

The contracts thus allow preferential pricing among others through:

a) The escalation mechanism.It's obvious that differences in these factors may bring differences in the short run. Our question is if these differences systematically favor contracts from one special country?

b) The composition of energy sources implemented in the contract and how their prices react to changes in the currency rates.

c) The composition of high- and low price consuming sectors

Comparison of gas prices

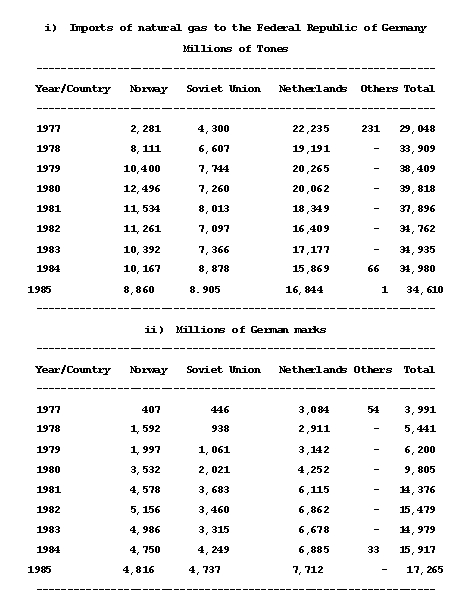

We shall look at the development of the prices on gas imports to West Germany; the biggest single importer of Natural Gas in whole Western Europe. As was shown in Table 2 West Germany imports gas from the Netherlands, Norway and the Soviet Union respectively. Dutch gas is taken in from the west of Anthem and Groningen, Norwegian gas via the terminal at Emden, while Soviet gas is taken in over the Czechoslovakian border to the west of Pilsen (the Megal pipeline) and through Austria. West Germany also acts as a transit country for gas, and pipelines for transporting gas out of the country goes from Saarbrucken to France and west of Basel to Switzerland and Italy.

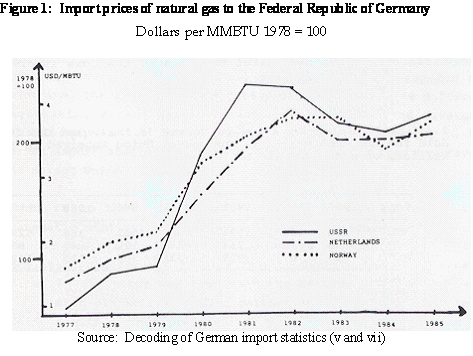

The source for my figures is official import statistics from Statistiches Bundesamt in Wiesbaden. The decoding method and the main features concerning calculations and methodic are described in a separate appendix. The unit of energy often used in gas contracts is the British Thermal Unit (BTU). German import statistics give prices in marks per ton. Conversion from tones to BTU requires quite accurate information regarding calorific values and specific weights of individual countries' gas. With reservations on the fact that re calculation factors may contain some inaccuracies and statistical errors in general, the figures show this development in prices for the period from 1977 to 1985.

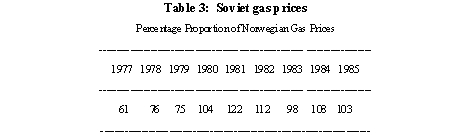

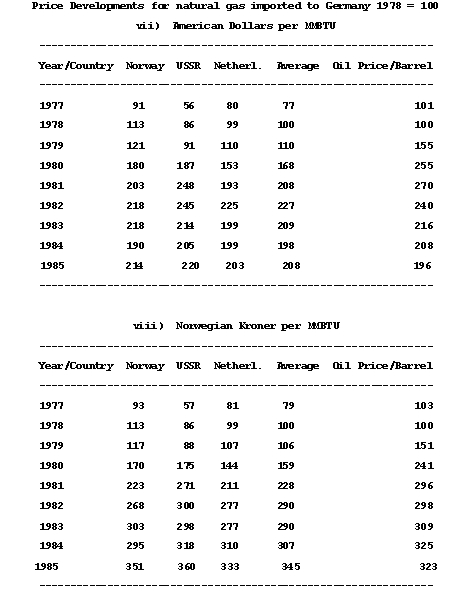

The figures show that when Norwegian supplies of natural gas started up from the Ekofisk field in 1977, prices were higher than both Dutch and Soviet prices. However, after the Soviet Union re negotiated its contracts in 1979 their prices overtook Norwegian prices and since 1980 they have largely remained above.

-

-

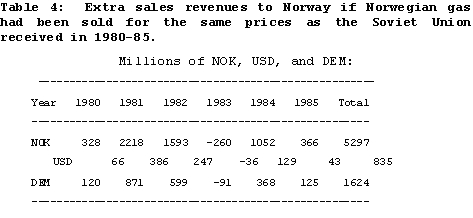

An obvious feature of the period is thus the growth of Soviet gas prices in relation to Norwegian prices, but it may seem as if the prices are converging on one another as time goes by. Since 1980 the difference according to German import statistics has been 4, 22, 12, 2, 8 and 3 per cent in favor of the Soviet Union. To a certain degree this cannot be said to represent very large differences, but because of the size of the sums involved they constitute large amounts:

Even though terms of supply in each contract may be different, as has been mentioned in accordance with definitions applying to trade statistics, import prices must be comparable. An example of a possible divergence from this, however, is that whereas prices in Norwegian contracts are determined at time of departure from the terminal at Emden, the point of price calculation in German statistics is located at the time of arrival, before the terminal. Thus the value of the cleaning process at the terminal is deducted from the invoice value. This means that part of the increase in value produced by forwarding the gas to consumers takes place in Germany. If such processing does not take place in connection with supplies of gas from other countries, this reduces the Norwegian prices in our survey in relation to these. However, the increase in value at Emden only constitutes approximately 1% of the contract price, so this difference will not alter the levels of the curves in the above figure. Nor will utilization of current values as done in Table 4 give an accurate expression of values lost in the period. However, the representation does give a clear impression of the fact that small margins soon constitute billions, thus making it important for exporters and importers to attract them to themselves.

The main conclusion which can be drawn from these figures is that so far Norway has not received any preferential treatment in the form of higher gas prices. It may seem as if prices are roughly speaking (over a period of time) more or less the same for all countries. The reasons for temporary differences may be different negotiating strengths/skills and/or willingness, and divergent escalation clauses in individual contracts. According to German import statistics these factors look as if they may favor the Soviet Union.

If it is so that the Russians' higher prices are not due to systematic statistical errors in the Statistisches Bundesamt and are not due either to negotiating skills or special (temporary) escalation clauses, it is difficult to explain the difference in prices in any other way than that the Germans regard the Soviet Union as an attractive trading partner and not as a burden to do business with. Thus preferential pricing goes in favor of the Soviet Union. Why? In an economic sense the Soviet Union as a market is more interesting and important to the Germans than Norway, even if we take into account Norwegian offshore activities and military equipment. Even though the absence of strikes is not due to the fact that people in the Soviet Union are particularly more content with their wages and working conditions than workers in the North Sea, the Soviet Union may also, from the buyers’ point of view, be said to be a country with "stable" working conditions. In addition, it is also possible that the Germans, as a part of their Ost-Politik, wish to trade with the Russians. Trade relations between countries create awareness of common interests, replacing knowledge of dissimilarities. They may thus contribute to relax tensions between both blocs in Europe.

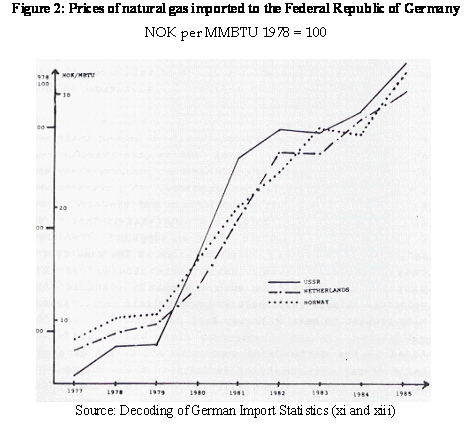

As a result of the fall in crude oil prices calculated in dollars, Figure 2 shows that gas prices also calculated in dollars, lagging to a certain degree behind crude oil prices, have also fallen. However, calculated in Norwegian kroner (or in another Western European currency) gas prices, like oil prices, have shown a steady rise ever since 1977. The fall in the price of oil both in European currencies and in dollars since the summer of 1985, and especially the winter of 85/86, will not fully affect gas prices in the European Market before some way into 1986.

Figure 2 is the same as the Figure 1 expressed in Norwegian kroner.

That is to say that the difference between them is only the annual

exchange

rate of the dollar compared to Norwegian kroner. Thus the comparative

relationships

between individual prices will remain as Figure 1. Corresponding

developments

also exist for prices calculated in other West European currencies.

Conclusions

If a purchaser wishes to employ sources that are unreliable when he has alternatives considered safer, they must provide him with advantages in "normal" periods, which compensate for those disadvantages he thinks he may get in periods of disruption. The probability of trouble and the extent of this trouble's effect on supplies must be weighed against the advantages he otherwise gains by employing such sources.

For commercial reasons importers desire to spread their purchases among several sellers. It is when weighing various types and degrees of risk against one another that purchasers may arrive at preferences among the various suppliers. In a scenario where one supposed that the Russians would turn off the taps, they would also lose their own currency revenues. What if instead they had the possibility of reducing Norwegian supplies? Then they would reduce energy supplies to Western Europe at the same time as they retained their income. Would their closing off their own pipeline not constitute such a dramatic scenario, that the political climate would make it possible that such a pressure was also brought to bear on Norway?

Added to the difficulties concerning evaluation of each exporter's degree and quality of security in their supplies (politically, military, technically est.), it would probably be extremely difficult for any purchasing government to discriminate openly between any of the sellers in price. Possibly it could easier be done in connection with volume and reliability of supplies. When the market grows it would be the country preferred that was first allowed to sell its gas. If a country was to receive any preferential treatment in the form of price, it would probably be in a more indirect form, for example through the purchasing countries financing parts of the field developments, through inexpensive loans, less visible commercial package deals etc. Such arrangements might in turn also lead towards the selling country to achieve greater stability in terms of supplies.

In a falling market preferential pricing could, however, have a decisive importance for the development of Norwegian fields. Considering the substantial costs involved in developing these, it would be of importance if Norway was guaranteed a certain price over a long period. However, one might call this a price guarantee, rather than a price premium, at least in so called "normal" market situations.

When the relation between oil (or more general: energy) and gas prices is established, the gas price will be determined on the basis of the current oil price. However, the higher the oil price, the smaller the gas/oil price-fraction have to be in order to cover i.e. the transitional costs for the consumers to leave oil in order to favor gas. Thus, contracts on future supplies of natural gas will imply expectations of future oil prices. The Statfjord contract signed in the early eighties was based on expectations of a rapid rise in oil prices from 1985 and onwards, whereas the now signed Troll contract contain expecta¬tions of slightly growing oil prices in the nineties. Like the Germans, who are renegotiating the Statfjord Contracts as oil prices did not show the expected rise, we will probably also see a renegotiating of the Troll Contracts if the oil price development does not follow the expected growth. If oil prices grow faster than expected, the contract will probably be adjusted upwards. If oil prices grow slower (or fall) in the nineties, the contract will probably be adjusted downwards.

The Troll contracts contain prices approximately on the 1985 level, thus a bit higher than the 1986 prices, but lower than Norway's initial expectations. This level seems to be what was possible to achieve with today's expecta¬tions of the oil price development, and thus a reasonable contract to sign for both parties. The market share will probably be one of the significant features of the ability of changing the contract in ones favor later if renegotiations are to take place, and the volume of the Troll contract are strengthening Norway's position in this respect.

We have seen that small margins constitute large sums. Thus it is important to all parties in the market that the margins are in their favor. Sellers may attempt to take part of the profits of the purchasing consortium, or also perhaps pass somewhat higher prices on to consumers. Given that prices remain more or less the same to each seller over a period of time, another way of looking at the gas market could be in terms of the sellers’ common interests. What about considering the coordinating of the sales policy to Norway, the Netherlands, the Soviet Union and Algeria, even if it will have to be considered as politically impossible at present? However, if the political connections of individual countries prevent parties from taking part in co operative efforts to increase common gas prices which they would otherwise wish to participate in, i.e. is the means of a common pricing strategy, the seller countries will be in a situation where they pay for political connections instead of gaining economic advantages from them.

With a group of buying countries gathered in one consortium and selling countries split, a market structure more or less made out of the present political situation, the West European Gas Market may be considered as an oligopoly on the sellers and a monopsony on the buyers’ side. Given that a monopsony have a stronger market position than an oligopoly, one could say that the political situation have led to lower prices in general to the sellers than otherwise could have been realized. In such a case the political situation implies preferential treatment of consumers at the expense of producers and not one producer at the expense of another.

APPENDIX

Calculations

In the Federal Republic of Germany natural gas is registered under a special trade number (27.11.910). The trade nomenclature used by the Germans is an expanded national version of the EEC area's common nomenclature, NIMEXE, which again is based on the Customs Co operation Council Nomenclature (CCCN).

As regards natural gas as an item of trade the total quantity and value of imports to the Federal Republic is given. Division into countries is not given in importation statistics in connection with the NIMEXE division. However, by employing statistics published by the Statistisches Bundesamt in accordance with various nomenclatures, one arrives at quantities, values and therefore prices of the gas Germany registers as imported from each individual country. Besides NIMEXE the Standard International Trade Classification (SITC), which is the UN's nomenclature for trade statistics, is utilized. They give goods in a different order than CCCN/NIMEXE do. Moreover, a special standard for trade groups is utilized in the German statistics. An exact description of how the various publications are combined has been published in Austvik (1985), Central Bureau of Statistics. For each individual supplier country the calculations give the following results:

The figures under "Total" have been checked against the quantities and values published in German statistics under the NIMEXE number for natural gas. I find some minor deviations in 1977 and 1984 but this is a matter of tiny fractions of the total and does not alter the main features of the final figures.

Not all natural gas registered as imported to the Federal Republic is consumed in the country. For example, 50 per cent of imports from Norway are re exported to France, Belgium and the Netherlands. See in this connection, for example, Austvik (1985, NUPI-Paper No 326). Our intention is to show price developments for imports of natural gas for each of the countries, and for this reason we do not pursue the gas to the "final" place/country of consumption. Thus, to the extent that differences in price exist in the different countries, these may have an effect on the average prices we have registered in the German importation statistics. To our knowledge the Norwegian prices to each of the receiving countries are similar.

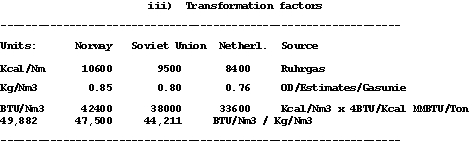

The above mentioned figures for quantities and values give us direct prices per ton. However, gas prices in contracts are not settled by unit of weight, but by unit of energy. Usually the prices in the contracts are settled per Millions of British Thermal Units, abbreviated to MMBTU. 1 therm corresponds to 100 000 BTU which again correspond to 25 200 Kcal in calorific value (OD's annual report). This means that there are approximately 4 BTU per Kcal.

The price of gas per cubic meter is found by multiplying the price per ton with the specific weight. The gas price per MMBTU is found by dividing the price per unit of volume (cubic meter) with the gas's calorific value per the same unit. We have set the values of individual variables for the different countries as follows:

By means of these factors we arrive at a conversion into prices per

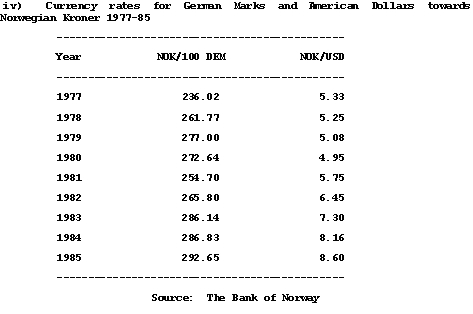

unit of energy (MMBTU). By means of the currency rates given

below

we also arrive at prices in the currency we desire: German marks,

Norwegian

kroner or American dollars:

The point of measurement was c.i.f. the German border. This means that all costs both in connection with recovery and transport up to the German border are included in the prices. Transport from the German border and internally in the country and any processing costs in the country have not been included. This gives us the following prices calculated in American dollars and Norwegian kroner per MMBTU. As the price of oil we have given the official norm price for Norwegian North Sea oil f.o.b. Teesside both in dollars and Norwegian kroner.

Corresponding tables may be set up as index rows. We have selected 1978 as the basis, since this was the first year when all three countries exported substantial quantities of gas to the Federal Republic.

References

Austvik, Ole Gunnar: ”Registrering av råolje og naturgass i norsk utenrikshandelsstatistikk". NUPI Paper No 326 July 1985 Norwegian Institute of Inter-national Affairs, Oslo

--- Den statistiske behandlingen av innførselen til og utførselen fra den norske kontinentalsokkelen". INO Paper No 58/1985 Central Bureau of Statistics, Oslo

BP Statistical Review of World Energy 1985

BP Statistical Review of World Gas 1985

Central Bureau of Statistics, Bulletin of Statistics, Oslo

Oljedirektoratets Årsmelding 1984

Statistiches Bundesamt, Aussenhandel nach Laendern und (Data Sourc Warengruppen

--- Foreign Trade according to the Standard International Trade Classification (SITC rev.II) Special Trade

--- Aussenhandel nach Laendern und Warengruppen (Spezialhandel) Fachserie 7, Reihe 3

.